Assume crash positions

Everything and everyone holding Bank of Japan bonds woke up this morning to the news that as from here on, they’re paying money for the privilege of buying and holding public debt bonds or keeping other deposits at the Bank.

That’s how bonkers things have become. But forgetting the lunacy of asking people to pay for the privilege of lending money to you – yes, even without that – the shock move being described this morning in the West as “risky” will, it seems to me, evoke some of the stuff the BoJ fantasises about…but also, all the stuff they have nightmares about.

Atypically compared to any Western country, Japanese citizens have traditionally held a lot of Japanese debt. But since the last time the BoJ pulled this stunt (September 2014) they’ve been massively overtaken by…..oh yes, the Bank of Japan. It seems to me obvious that the 20% share of T-Bills owned by the Bank will zoom upwards. Insurance companies own about 19%, financial institutions 13%, and overseas investors (as ever) quite low at around 8%.

So far, the few people awake I can talk to have as many theories per minute as they have heartbeats, but I’m sticking to the commonsense line.

What’s happening here – surely – is that the Central Bank is now lending money directly to the Japanese Treasury and all at a loss.

Can this really be a very clever idea? Well, the Government borrows free money (so it might cut consumer taxes to encourage reflation) and the Yen effectively devalues….which it already has in Asian trading….and to pay for all this, the BoJ prints more money which produces the 2% inflation that Abenomics desires.

Sooooo, consumption grows, exports increase and deflation is reversed. Excellent.

Um, not really.

Generally, what this represents is yet more financial pointyheads firmly of the belief that monetarist sleight of hand is a solution to economic problems. I don’t care what anyone says, printing money and entering a potential spiral is never a good idea.

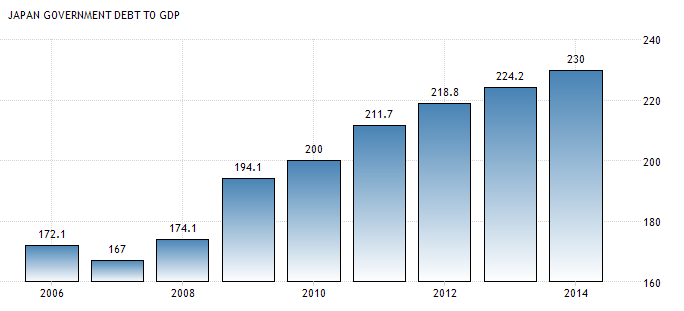

Then there is the size of Japan’s public debt. It is, as the euphemists remark on ‘an upward path’, which is not a good direction:

It stood two years ago at 230%. The IMF estimates it is now 250%, and last July 23, the Lagarnauts declared the debt to be ‘unsustainable’. Japan has by far the highest debt ratio of any developed nation – Greek debt stands at around 190%, but quite a bit of that is the result of “help” from the Troika. Japan managed its figure without any outside help at all.

A third consideration is our old friend the zero sum game. A cheaper Yen has been achieved, and I will gladly be a candidate for monkey’s uncle if this doesn’t produce a retaliation from Beijing and others by return of post.

Now this is where the broader ripples might get tricky, in the light of late of a deliberately weakened dollar. In total, some 46% of Japanese T-Bills are owned by commercial and public institutions there….not counting the insurance companies, who similary need to make a turn on the money. As the BoJ hoovers up this costly lending (or income from government borrowing, depending on how mad you are) a good two-thirds of the money could easily fly to safety…..aka, the US Treasury – and that means the potential for negative yields there plus a strengthening Dollar.

What then? Sounds to me like Janet Yellen has a new place to sit in between the rock and the hard place. I think one might call it a spike….but that means a restrengthening Dollar. My initial thought is that it will give the US Fed a ready-made excuse to reverse the December rate-rise.

Last but not least, although very few observers saw this coming, as I wrote earlier this is not a new policy: it is an old policy applied to the failure of the one of the worst ideas of all time, Quantitative Easing. It looks and feels like Abenomics, having reached the end of the road, is going round in circles.

That means more doubts about central bank efficacy and new ideas. Assume more turbulence.