…as Greek youth unemployment heads for 70%

Sir Andrew Cahn…”EU has generated prosperity”

Sir Andrew Cahn…”EU has generated prosperity”

That’s what Reuters says. Which just goes to show you how utterly pointless confidence indicators are when you use a sample of incurably optimistic clowns who caused most of the trouble in the first place. We can ‘put Cyprus behind us’, say there hasn’t been a suicide in Athens for 36 hours, or rejoice at the coming of the Carneyvore to the Bank of England: confidence in the EU is beyond false: it is pure fantasy.

Now that Cyprus has been tucked away onto page 13 by the subeds, we would all do well to keep track of how all the neighbouring carnivores are being rewarded for their cooperation with the Brussels-am-Berlin heist. Last Thursday, The UN Secretary General’s Special Adviser Alexander Downer hosted a dinner between President of Cyprus Nikos Anastasiades and the Turkish Cypriot leader Dervis Eroglu. Mr Downer was at pains to point out that the dinner did not “constitute an intention on behalf of the United Nations to resume the direct talks between the two sides on the Cyprus problem.” They were obviously just there for the beer.

Greeks, of course, see only one problem on the island: the illegal northern part invaded unlawfully by Turkey a long time ago. They would like the Turks to bugger off, and it isn’t an unreasonable request: they do, after all, have no right (in a sovereign sense) to be there at all. However, although the meal was most emphatically not a precursor to new negotiations, it was a bit of a Downer when UN-Man said “…a careful preparation must be done before negotiations can resume….The main thing is to get the preparatory work done and done properly, the two sides obviously have to do that.” Er, not if they have no intention of resuming direct talks they don’t.

You can see this as nothing at all – three chums and their wives having dinner – or not. I’m in the ‘not’ camp. But if you think dinners about no talks to prepare for not having talks is a tad surreal, try this new advice to investment clients from Citibank:

‘Although we still see risks of Greece leaving the euro in the next few years, we have removed “Grexit” from our central scenario in 2014. The governing coalition looks somewhat less fragile than we previously thought and, with key legislative actions for 2013 behind us, we do not see major triggers for the coalition to break down in the near term. Despite a significant drop in living standards, social unrest that could destabilise the government remains contained so far, although risks of an abrupt eruption remain.

Yet, the Greek public debt is still on an unsustainable path in our view, likely to approach 180% of GDP by end-2013, and the economy remains in recession. But the recent slightly better compliance with the fiscal targets and, in general, a better cooperative stance by the Greek government towards international lenders should make the lenders more open to some additional debt relief – in the form of OSI – later this year or in 2014.’

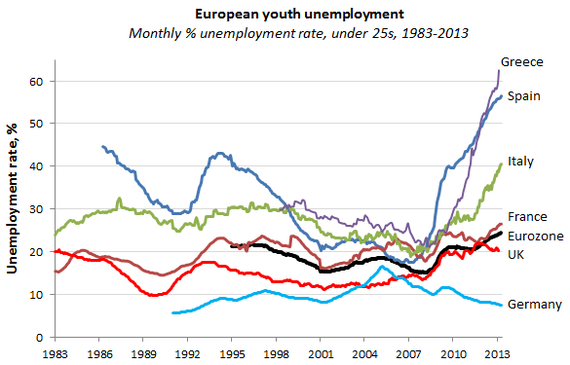

It reads a bit like advice to folks living on the slopes of Vesuvius, except that the impression of dormancy is slightly marred by the tell-tale trickle of molten lava coursing through Mrs Cicero’s kitchen. There’s no economy to speak of, no young people in a job, no social unrest tonight at 3 am, no way the debt can be paid back, no chance of the projected tax intake being reached and – best of all – no major triggers are apparent. It’s all about taking the triggers out of the guns in the end. Guns with no triggers don’t work. Somehow, I get the feeling that Citi didn’t take this graph fully into account:

As you can see, all the Clubmeds have rocket trajectories of youth unemployment suggesting they’re set fair to leave the stratosphere some time soon, on their way to Planet Gogg. Greece’s rate has been growing at about one percentage point a month, and will at this rate hit 70% before the year is out. Thank God we took the triggers out of the guns. Zero Hedge has a marginally different view on how things are progressing:

‘Germany prospers. Everyone else suffers. The EU unemployment rate hits 12.2% which is a concocted number far below actuality but that is what they say, that is what is believed, but our old friend reality always has a funny way of showing up when you least expect him. In France they now have 3.26 million unemployed with two uninterrupted years of monthly rises in their unemployment rate and a 1.2% increase from March. Nearly 337,000 more people are out of work in France than there were when Hollande was elected in May 2012. Unemployment is Spain at 26.8%, some 6.2 million people out of work while the economy has shrunk -1.3% in the last two quarters. Italy’s economy is projected to shrink by -1.8% this year according to the OECD while their unemployment rate hits 12%, a thirty-six year high. Besides Germany these are the pillars of the European Union, and that union is crumbling.’

On the other hand, said Bloomberg, ‘Economic confidence in the euro area increased in May, adding to signs the region is beginning to emerge from the longest recession in the single-currency era’. Time for someone to tell us whether it’s a butterfly emerging from a chrysalis, or Rosemary’s Baby shooting past the clitoris.

I can add some personal colour to the French picture. Everyone is looking for extra work and everyone is evading tax. The annual inflation rate in France was recorded at 0.7% in April. It’s a joke: everything is going up in price. And this of course brings us back to my favourite subject, indeflation. Since I and one other invented this word about three years ago, slowly but surely more and more scholarly articles have begun to accept that the flation for which we’re heading will be both fish and fowl: but in a nutshell, it seems to me like everything the citizen gets or buys is going to inflate in cost….while most of what he or she sells, eg labour, is going to deflate. Call me old-fashioned, but that has a sort of Weimar ring to it.

As I predicted here some months back, Canadian Mounted Currency Policeman Mark Carney moves into the Bank of England this month, his avowed intent being to crush the value of the Pound. Feels like there’s a fair amount of inflation inherent in that one. I’ve been in a minority of one about the CMCP riding into town to sort out Blighty following his hugely successful Canadian tour, in that his thinking seems to me to have all the profundity of an Iraqi puddle. But now at last someone agrees with me.

Adam Button at Forex Live insists that Mark’s contribution to Canadian stability “has been grossly exaggerated”:

‘It’s tough to read the BOC statement from early September 2008 and give Carney any sort of credit as a great central banker. Dislocations in credit markets were overwhelming at the time, but Carney said ““The course of the U.S. economy and the ongoing turbulence in global financial markets – have evolved broadly in line with the Bank’s expectations”.’

Three days later, Lehman collapsed. Carney abruptly switched tack after Lehman collapsed, but Button thinks he didn’t hit the panic button hard enough until December – by which time, the global economy was on its knees. “In truth, he benefited more from Canada — a country that coasted through the crisis because of a commodity boom and fortuitous government banking policy — than Canada benefited from him,” Mark concludes.

So then, we’re all set for the big turnaround here in Yerp. There are green shoots here and there who think the crisis is receding, but then they are plant life. And my Daffodil of the Week award goes to Sir Andrew Cahn, who writes in today’s Telegraph thus:

‘Institutional structures are better than passing political policies as a route to keeping the peace. Britain is safer because of the EU. Not only is EU peace taken for granted, but so is the prosperity it has generated. In Britain, for example, many now see the eurozone as a burden on the economy, arguing that we would be more prosperous outside it. It is difficult to understand this argument.’

Which is fine Sir Andrew, because I find it impossible to understand your conclusion. Sir Andrew Cahn, by the way, is vice-chairman, public policy, of Nomura, and a member of the World Economic Forum’s Global Agenda Council on Europe. Yes people, we are in safe hands.

Last night at The Slog: EU contingency planning if food becomes unsafe, suddenly.