The idea of elegant simplicity was abandoned in favour of deliberately obtuse complexity decades ago. For many years, this was merely irksome. Now – in terms of global complications – it has entered a marriage fashioned in Hell with technology. In such a situation, nobody stands the ghost of a chance of understanding what’s really going on any more.

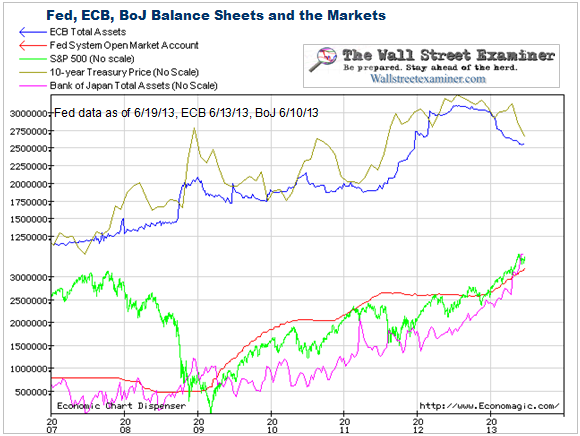

Do you understand this chart? I know a guy in New Mexico who does. But given its impenetrable nature for 97% of humanity, is it any way to run a railroad called Planet’s Economy Not In Shape (PENIS)? I think not. Here are some prose examples:

UK stock market breaks its fall after mounting worries over US and China hit global shares and hike government borrowing costs

Do you REALLY know how your pension is invested? Safety-first approach knocks 5% off ‘lifestyled’ pots as bonds slump hits

The 15-year gilt rate is, in effect, the wholesale price of an annuity

I have bad news for you, folks: this is rumoured to be the easy stuff. Early on in my career, a famous adman said to me, “If you can’t explain something in one minute, chances are it’s a bad idea”. I still consider that to be a truism today.

I have good news for you folks: I could teach you a good 75+% of this bollocks in a day. And so, in the spirit of keeping things simple, here goes…..

1. All governments overspend. This is because it isn’t their money.

2. All bankers invent ways to make paper seem valuable. This is because they don’t understand wealth creation.

3. All interesting people are bored by finance. This is because it is interminably boring.

4. Tediously sociopathic crooks take advantage of the boring dimension of finance to cheat people.

5. When governments overspend, bankers come to their rescue. When bankers screw up, governments bail them out. It is a mutually beneficial relationship that leaves the taxpayer out completely…until it comes to paying the bill.

6. Once upon a time, insurance and pension providers did not invest in the stock markets: they put our money only into things like government bonds, which were rock solid.

7. Once upon a time, governments didn’t piss away taxpayer monies, and so their bonds were rock solid. Then they got grandiose ideas about spending on stuff that could never pay back. And then insurance and pension providers began to invest in stock markets. And beyond then, insurance and pension providers spread their risk by investing in both bonds and stocks. This was a little like hedging between the Titanic and the Lusitania.

8. Pretty soon, sovereigns, institutions, companies and banks began saying they had to do profoundly bad stuff – because they had to consider the shareholders….aka the insurance and pension providers.

9. Into this melée came the hedge funds and light-speed traders, to overlay profusion upon confusion. And at a height somewhat above them, people slicing up promisory notes called derivatives were busy making two acres of a Kansan maize crop worth $3m to a small building society in Scotland.

10. And so we arrive at today, where everyone buys and sells everything. Or, to be more precise, everyone bets on the value of everything – knowing only too well that at least half the time it’s worth three-fifths of nothing. This applies mainly to the stock market, but also to the bond markets. Betting on the bond markets is theoretically good, because if the issuers default, there’s always the insurance to bail you out. Those are, however, the same insurance companies up to their necks in 8 and 9 above. And if the defaulter is Greece, the ECB won’t admit it’s defaulted, and thus tells you to go screw yourself. So everyone is angry almost all the time, and pretty darned discouraged when the ‘essentials’ that are supposed to guide the prices and yields turn out to be not just awful, but also completely unrelated to the prices and yields.

The trouble with elegant simplicity in 2013 is that it gives the game away every time. Only complicated, multifaceted, hypothecated, quantitative, and derivative can keep the troupe on the road just one step ahead of the creditors. Big and complex is bad. Small and simple is good.