Something is afoot, and the Thinkers know it

If I had a Pound for every reassuring élite smile and scared young face I’ve seen around Europe and the UK over the last eighteen months, I would be a rich man indeed. It is very odd to watch Samaras on the TV mouthing bromides one day, and then be told that Civil War is coming by a senior and serious Greek professional the next. There was something eerie about Italy last Autumn, and there is something vaguely off-key – even slightly hysterical – about French life at the moment.

This odd mix of resigned ‘Thinking Class’ expectancy and Sovereign fear is not just my imagination – of that I’m now almost certain. In London, there are people in influential positions genuinely scared about what the Met Police might do next, where the BBC DJ farce is going, and what will happen later this Spring at the end of the Newscorp trial. Detectives working on the Elm House investigation are dropping heavy hints about serious dissension in the ranks if the guilty in this case are allowed to escape yet again.

A good, highly experienced and professional journo friend confided to me the other day that the Conservative Crown lies askew on the King’s head concerning a matter of which few people are, as yet, even aware. Meanwhile, the real Royal heir is being moved quickly into a thinking role alongside Mum…having already last year secretly brokered a level of press privacy for the Windsor Household that is unprecedented in modern times.

The Sun headline is ‘Rich and powerful tremble as established order on knife-edge’.

And it’s odd how, once the thought has entered one’s mind, even the endless stream of ‘turning the corner’ tripe (and the most risible banker insistence that we’re all paranoid) simply can’t remove the scent of stink bombs from the nostrils.

I ignore any and all reassurance emerging from the City these days on principle. I have heard so much self-serving rubbish and envelope-pushing ‘natural order’ drivel spouted by City types and bankers over the years, that I have often searched for Wildesque ways of describing them. Bear in mind, my experience of these berks goes all the way back to the 1970s at Barclays, and then via various Merchant Banks and Insurance companies before returning full circle to Barclays again (1988) and then what was then the Halifax (1992-9) as it morphed predictably into the basket case formerly known as HBOS.

The best one I’ve come up with to date occurred to me yesterday while raking up grass cuttings: ‘A banker is a person who cannot tell the difference between the merely subjective and the really objectionable’. One I met on holiday four years ago, for example, tried to explain to me why banking firms couldn’t possibly make any extra money out of QE, and that I’d see – yes I would – soon enough how Ben Bernanke and others would have things back to normal again, and no he didn’t think that 1% of Americans owning 50% of the wealth was at all lopsided, because in the end “talent will always out”. So that was me put in my place, then.

Another corker of a conversation was one with a chap to whom I’d suggested that all talk of recovery (even if it wasn’t pure fantasy) was rot anyway because first, without QE it wouldn’t have got started – and didn’t his sort think markets should never be tampered with by bureaucrats? – and second, they then had the brazen nerve to count QE in as a form of economic activity to make growth look better.

“What’s wrong with that?” he asked (actually he yelled, but I’ve put the question mark in now) “If you think it’s the f**king elephant in the room, than let’s count it as in the room”.

It was a witty answer, and I could see he was well pleased with it. “It isn’t just any old elephant in the room,” I heard a woman’s voice reply to my right, “It’s Dumbo. And Elephants with wings only fly in cartoons”. I fell in love with her instantly, but sadly she’s married….to a very nice bloke, more’s the pity.

But the portents of doom turn up in the oddest of places.

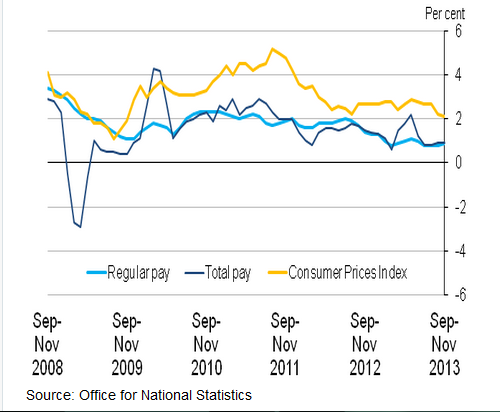

The other day, while looking at a salaries v prices chart, I spotted something that I wasn’t looking for, but it was intriguing enough to make me think further about it….and then ring the Office of National Statistics about it. This is the chart in question:

The lines to look at there are the dark blue (total pay) and light blue (monthly salary). The difference, by and large, is bonuses. They tend to happen at the end of December or end of March…depending on whether the company has a calendar or tax year fiscal.

The lines to look at there are the dark blue (total pay) and light blue (monthly salary). The difference, by and large, is bonuses. They tend to happen at the end of December or end of March…depending on whether the company has a calendar or tax year fiscal.

As you can see, there are some quite major gyrations of bonus up and down. So I rang David Bradbury at the ONS media centre (nice man, very helpful, on the ball) and asked if he could tell me whether these were mainly private or public sector. “Overwhelmingly private” he said, and then went through some of the huge uplifts involved. It was obvious to both of us that by the size of the jumps, they must be overwhelmingly City bonuses.

Further confirmation for this comes from the timing involved. You can see that in the last quarter of 08/first quarter 09, the total pay of the MoU’s plummets compared to expectation. This was at the height of the mess, when bank managements were chucking traders, section managers and even bigger cheeses out onto the streets with their personal belongings. The degree of taxpayer bailout that might be available was to say the least of it unclear. So this wasn’t bankers restraining themselves out of duty to the Government: it was bank management fearful of actually going under. It was a time of Northern Rock, Bear Stearns, and Lehman Brothers. Although he doesn’t like to remember it now, it was also a time when Barclays’ Bob Diamond was pleading with Ministers to bail everyone out…before he eventually found some seedy Arab friends to play with, and then changed his tune.

But look what happens in the equivalent November09/March10 period a year later. Brown, Balls and Darling have given them all our money, and their Conservative mates will soon be in to feather-bed them forever….so the bonuses go soaring upwards again back to the same levels.

The moral (if that isn’t too ironic a word) is simple: when it’s their money, no bonuses. When it’s our money, unlimited bonuses.

However, none of this is new news. My sole purpose in reaffirming the sh*theaded nature of City bankers now is to explain a modus operandi, a rule if you like: bonuses only get smaller when the bank’s management is genuinely fearful.

I can tell you categorically that, within days of being in office, both Cameron and Osborne did a ring-round of the main bankers to try and read the riot act about bonuses; it hadn’t taken long for Fleet Street to smell that it was bonuses as usual. The answer they got was a resounding raspberry – especially from Bob Diamond.

But the above chart’s blips and dives since that time suggest that, in fact, there has indeed been a significant reduction in bonuses paid. 2010/11 was much smaller, 2011/12 was almost devoid of bonusing, and 2012/13 was better…but still under half that of the fat years.

Now all this time, we’ve been told that the banks are sorted out, balance sheets have been repaired, toxicity has been offloaded, and derivatives netted. But bank managements have paid out a lot less. Even they, by now, have realised that the era of bailouts has gone – hence the idea about turning customers into creditors next time.

I submit that less has been paid because the boys in the penthouse bar know that things are far from sorted. I submit that they’re fully aware how – even with bailins – next time it could be the End of the World Café.

That’s just one smallish thing: a confirmation of other equally compelling trends. The craze for glitz-brick top end property, the rush to buy arable farming land, the uncanny degree to which most of the national political and banking élites and big-throw dice directionalisers seem to have future horizons that don’t stretch beyond May 2014. I’m referring to tips about Hillary Clinton expecting a crash “in the summer”, about the blasé Brussels-am-Berlin attitude to Greek default on the one hand, and Draghi’s desperate brag-hand plot in relation to Italy and Spain. About Cameron playing for time on the EU in/out referendum. And a host of other titbits here and there down the line.

I don’t say that anyone is sure things are going to go pear-shaped. I merely suggest that preparations are being made in earnest. Water cannon purchases by metropolitan police forces up and down Britain, for example, are not what you’d call normal Plod behaviour. I’m informed (as are thousands of others) that riot control hardware budgets have also been massively upped in the US. I know for a fact that sales of such hardware at one British firm are through the roof…and widely international. The NSA scandal itself, I’m sure, is part of the same fearful desire to have Government ears to the ground, and portable/expandable crowd railings at the ready.

Nobody is displaying this urgency (I’m told) more than Boris Johnson. I could of course be naughty and say he has more to fear than most, but he clearly has given Home Secretary Theresa May one or two things to think about recently. In private, London’s Mayor thinks serious violence and a terrorist attack are very real issues. And he is, without doubt, sailing with a very wet seat of the pants on two particular issues.

A major staging post for this sense of mine about nervous leaders was the remarkable switch of attitude by Janet Yellen three weeks ago. Never in four decades of watching people in the public eye have I seen someone so suddenly morph from dove into hawk when it came to easing the intractable US unemployment problem. Suddenly it was “Let’s hear it for the taper!”

And there is more. I was sent an intriguing piece from the FT’s Izabella Kaminska the other day, talking about how the leaders in Beijing are clearly aware they might be in for serious unrest. Two days ago, Zero Hedge reported the discovery of a massive (as in $4trillion) siphoning off of money for Chinese bigwigs in various Caribbean and other offshore locations. Words like Nazi gold and South America spring to mind.

I was already wondering about the Chinese gold thing before these things popped onto the radar screen. I don’t buy this ‘diversification out of US debt’ bollocks as the reason for Beijing’s voracious appetite for the shiny stuff. Regular contact Butch points out that China has enough money swilling about to ride five US defaults. But still they keep buying the gold, still they keep enlisting South African help to get it out of the ground. Why? Is it for them? Or is it a bargaining tool to be used (perhaps) as the seed capital for a massive programme designed to stave off Chinese worker unrest by investment in housing and other welfare?

Yes, I know it all sounds wacky. But we have been a long, long time putting this day of reckoning off. A hundred different countries round the world on every continent – from Ukraine to Greece, and from Argentina to Belgium – are in a parlous security state with a simmering citzenry.

A report came out of Belgium on the French news last night about French citizens there being told all bets were off about welfare for them or immigrations for others…EU ruling or no EU ruling. Marine LePen, Geert Wilders, New Dawn and our very own Nigel Garage are all of a similar mind. I reported earlier this week about Hollande’s sudden conversion to drastic spending cuts. We have Tokyo grappling with Chinese claims, economic meltdown and nuclear irradiation while buying tons of Italian debt bonds, and yet Italian banks finding more $30bn worms in cans. Today’s El Pais is covered in graphs about the rise and structure of unemployment…all of which gives the lie to Rajoy’s constant cries of emergence from recovery. And the Syrian ‘peace’ conference has thus far been anything but.

I realise that tonight’s piece feels like a bit of a ramble, but in all truth it isn’t. There is a confluence of complexity and collapse coming our way – some of it self-inflicted, some of it sod’s law of serendipity. Sovereign defaults, global derivatives, economic slump, social unrest, European chaos, Russian social and energy instability, manipulated markets, collapsing legal systems, new Islamist strategies, energy desperation, strident whistleblowers, dirty linen, ubiquitous corruption, and – perhaps most disturbing – increasingly unlikely interpretations of events from those on high.

I do not think that, in any way shape or form this sense of unease is felt among the more media-distracted and apathetic orders who are increasingly obvious in the better-off nations of the West. But behaviours in relation to spending and investing among the upper middle and top income/education brackets do strongly point to a mindset that has now taken serious hold among the planners and the thinkers.

And so, having ruined your night’s sleep, I will leave you with one thought. You can depict a thousand scenarios in which the destruction of gold’s value looks like a dead cert. But you cannot, ever, stop human beings from trading in the best hedges against currency destruction….and bullsh*t aside, by far the best of these are gold, followed by cultivable land with water on it, and then property. Better (people will always argue) to have real things for barter, food and accommodation, than €40 trillion in paper fit only for wiping one’s backside. And not even very good at that either.

Earlier at The Slog: Why the EC and Italy have handed UKip half a million more votes