Revealed: how the banks really are bigger than the Sovereigns

Which would you say is the more ‘valuable’ in these pairs?

UBS and Switzerland; BNP Paribas and France; Barclays and the UK; RBS and Scotland; Denmark and Danske Bank?

Now obviously, we’re comparing apples with pears here. Or crooks with workers, depending on your outlook. But the point is that, although as assets countries are bigger than their banks, in almost every case, the big banks are far bigger than the annual GDP output of the countries in which they’re domiciled….and far, far bigger than the State.

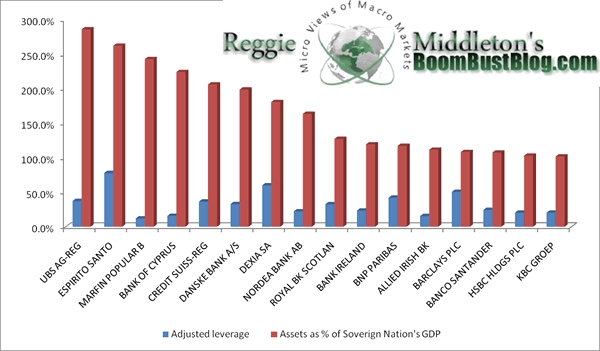

UBS, would you believe, has assets of a staggering three times Switzerland’s GDP. BNP Paribas assets are an equally incredible 1.4 times the GDP of France. And Danske Bank is sitting on stuff some 200% the value of Denmark’s total annual output.

The bar-chart tucked away in an excellent article at the US site Zero Hedge (see above) shows you the whole shebang at a glance. But this very telling chart about the assets of our banks versus the earnings of our States (compiled by respected contrarian market commentator Reggie Middleton) becomes rather more sinister when we make a straight comparison between bank assets and government assets and income.

Here in the UK, the Government’s total tax take is around £550 billion – 37% of GDP. Barclays’ assets here are three times that. At the last count, UK Government assets stood at around £340 billion. Barclays thus has nearly five times the assets that the Government has. And that’s just one bank. Hardly surprising, then, that when Bob Diamond says “Jump!”, the Coalition exceeds the Olympic pole vault record…..without the pole.

Now imagine the UK as a household, using Barclays as its personal current account bank. No 1 UK Street has an income plus savings totalling nearly £900billion. Barclays has an income plus savings of getting on for £1.7 trillion.

But the main difference, of course, is that Barclays made a profit of £11.6 billion, not a thumping great loss of £155 billion, as Britain did. And the UK’s national debt far exceeds anything Barclays could come up with.

So then, when your bank says that it’s going to pay out a relatively small sum in bonuses, what are you going to do: have a fit of moral vapours, or just sort of fade away quietly, while telling all the members of your family that there’s no point in bashing the bank? Yes, quite.

Now all of this might explain why, when Freddie Goodwin realised his star-trucking lifestyle was doomed – and he and his mates needed money pronto – he felt perfectly able to swan into 10 Downing Street and say, “Look here McFattie, we’re going down – and if we go down, you’re going with us. So bail us out, or else”. (At the time, I knew one of the people in the room – and trust me, this is pretty much what took place.)

But the irony is that we – you and me – have not only bailed out a collection of morally damaged kids involved in a global pissing contest earning far more than us; we have also been conned and cajoled into using our incomes to do this – even though their assets are far greater than ours. This is rather like Simon Cowell shaking down the residents of a Glasgow tenement because he lost the rights to X-Factor in a poker game.

Earlier today, The Slog reported Neil Barofsky’s refreshingly forthright comments on the gargoyles of Wall Street. On February 17th this year we reported at length about who really benefited from Zirp and QE. On March 9th this was followed up by an equally well-documented piece about the real motives of our central banks. Predictably, all these were criticised (usually at a pretty infantile level) by active or former bankers whose delicate feathers had clearly been ruffled by the truth. This is no different to the hate-mail I got from Lehman senior management when, in 2006, I forecast that the bank was so dependent on M&A for its income, in any kind of downturn or panic it would struggle to survive.

German banks are exposed to Greek debt. French banks are exposed in Spain. Spanish banks are exposed in Portugal. British banks are exposed in Ireland. And RBS is so exposed to Russian fraud, I don’t even like to think about it – especially as my gold note is with them.

In the final analysis, there really is no such thing as soi-disant ‘sovereign debt’. There is only bank lending, bank default swaps, bank derivatives, bank stupidity, bank hubris, bank bets…in fact, as Vince Cable said, spivs in casinos. For this, he has been excoriated as some kind of Trotskyite nutter. But as we’ve said many times before here, he is merely articulating the disgust and anger of what is still (I like to believe) a British moral majority. I’m not that keen on Vinny, but as long as he’s the only one with the bottle to take on these bastards, then he’s the man for me.

{kind=link}

{kind=link}