As the Wall Street Journal opined last October, ‘Superlow U.S. interest rates are squeezing bank profits, complicating the industry’s nascent recovery from the financial crisis…..Banks will be forced to consider new ways to make money by changing the services they offer, industry observers said.’

As the Wall Street Journal opined last October, ‘Superlow U.S. interest rates are squeezing bank profits, complicating the industry’s nascent recovery from the financial crisis…..Banks will be forced to consider new ways to make money by changing the services they offer, industry observers said.’

Or by extorting the money from customers. It’s becoming clear now that this is precisely what the banks have done – certainly in the UK. Our FSA declares that ‘more than 90%’ of the complex interest rate derivative loans sold by banks to small businesses were probably mis-sold – and this doesn’t include the naked embezzlement scam in terms of borrower asset valuations. To bring this down to a micro scale beyond even SMEs, the worst offender RBS is also routinely cheating its personal customers. The following is typical of emails I get on a regular basis from those unfortunate enough to have taken out savings products with a bank – lest we forget – they own:

“I took out a bond one year ago , on the [RBS] manager’s instructions that it will pay me 3% on maturity, so I invested £40k. The year is up and they only paid me £725. It should be £1200, how do they get away with it? I have all the paper work and the bond cert which clearly states 3%. I have complained, but they kept me holding on 45 min’s last time. I wrote and have been on the Internet – is this fraud? I think it is: what is my next step?”

To be honest chum, I’ve no idea. But what with ‘glitches’, stealing, mis-selling, Zirp and cheating savers, we get a pretty clear picture of desperation. It’s the same picture we see in the EU at central bank/sovereign level, and it’s the picture one gleans daily from professional traders, investors and Wall Street sources in the US.

The obvious nature of the desperado strategy (and brazen or not, it is being very carefully planned) is worth taking up a few paragraphs to review.

I’ve been blogging a lot recently about how most of the macro pretence has been abandoned by the élite survivalists of late. I suspect that, as we’re getting down to the short strokes now, there’s neither the time nor the inclination to bother hiding it any more; and also, the MoUs are confident that very few people are paying attention anyway.

Little else could explain the process that’s unfolding before those with their eyes open. The gold price continues to bobble along under £1700, but its every challenge of higher values gets quickly capped. Central banks want gold in as many bank balance sheets as possible, and the Chinese are buying the stuff like there was no tomorrow. So it’s in ‘everyone’s’ interests to keep the price down – that is, everyone in the élite. With that much macro demand (and every investor in the world desperate for a safe haven) the price should be around $2200+ by now. Only deliberate manipulation would account for its Friday close at $1667.

Despite huge amounts of Belgian, French and German euros being switched into the Swiss franc, Zurich itself admits quite openly it is selling the SF to keep it ‘cheap’. EU citizens are flogging their euros because the euro is a basket case, but the euro’s value has been soaring over the last fortnight: its value this morning is £0.87, heading back towards the levels of 2010. This is because the ECB is buying euros, and the Bank of England is selling sterling – for reasons of currency and export credibility respectively.

The value of anything can be fiddled: in March 2008, the New York Fed advanced the funds required for JPMorgan to buy investment bank Bear Stearns for pennies on the dollar. The deal was particularly controversial because Jamie Dimon, CEO of Morgan, sits on the board of the New York Fed and participated in the secret weekend negotiations. Over that same weekend, several banks (JPM included) were holding out on money they owed Bear Sterns. The investors in (and staff of) the victim bank were, without question, cheated.

As most of us remember vividly, the value of Greek debt bonds turned into a fiasco early in 2012, during which Mario Draghi’s European Central Bank (ECB) blatantly subordinated bond investors. From 2005 onwards, we know now that the Libor rate was deliberately understated with the connivance of both the governments and firms involved in the Libor trade. Our old friend RBS has set aside funds for an £500m fine for rigging Libor rates, but we own it – so it’s our money that’ll pay off the criminality. And just so we’re clear, no bankers were harmed in the making of this decision.

The stock markets are ludicrously high because of QE. Entire ClubMed countries are ‘solvent’ thanks to taxpayer bailouts, illegal interbank loans, and currency printing: the Italian MPS scandal will, I think, reveal more than the tip of this deadly iceberg we’ve seen to date.

Although this might be more detail than most readers need, it is important to show specific evidence backing the idea of an overall policy being adopted by the financial establishment. Via a really quite startling combination of taxpayer gifts, customers getting paid nothing, businesses being defrauded, customers cheated, rates bent, currency massaging, capping gold, pumping up the stock market, toxic debt being bought by the citizens without being asked, and inflating away Western debt, the powers that be answerable to nobody hope to keep the show on the road.

The process has been taken a stage further in recent weeks by an attempt to manipulate sentiment about what lies ahead. The VIX measure purports to show the level of concern about volatility in the markets. But it has a ‘sister’ betting shop, the VXX, which allows punts to be made on what future sentiment will be. I’ve posted about this before, but Zero Hedge had an interesting snippet yesterday about where this is going:

‘….courtesy of the reflexivity of the market, in which the underlying is driven by its synthetic derivative (for a detailed explanation of how that works just ask Bruno Iskil and how massively mispriced various IG credits were thanks to his whale trade in IG9), the VIX itself is being pushed around by the VIX futures itself….’

How bizarre is that? You bet so hard on the VXX about the VIX being calm, it becomes calm because of expectations about the future. Amazing: the self-fulfilling prophecy in reverse. Somebody (and it’s impossible at the moment to prove exactly who) wants a low volatility score so that, when the next load of optimistic bollocks is handed out to mass investors, the authors can say “And behold – the market professionals agree with us!”

~~~~~~~~~~~~

There are two points that I find overwhelmingly important in this context. The first is that, between now and the summer(ish), those pulling the strings in this puppet show want people to stay calm so they’ll stay put: in the stock market, in sovereign bonds, and out of gold. They want a clear run at what they want, if you follow: happy shareholders, low borrowing costs, and cheap bank balance-sheet restoratives.

But it does make one ponder WTF they want after that. Or if even they know WTF they’ll get.

Second, the entire scheme is based on one decidedly dodgy assumption: that Zirp can be maintained at will for as long as is necessary. As I will now try to explain at some length, I don’t accept this But the MSM buys into the idea almost without question. ThisisMoney, for instance, quoted the Investec view with some confidence this week: ‘Philip Shaw, chief economist at Investec Securities, says the market’s prediction is similar to his own. “It’s unlikely that the monetary policy committee will want to see rates rise in the short term,” he said, “We think the first move will be in an upward direction. We don’t see a rise for quite some time – the third quarter of 2014…”

Excellent. Nothing to worry about. Nothing can blow us off course. We are in control. There will be no ‘events’: we will not allow them to happen.

But what the Bank of England monetary policy committee (MPC) wants, and what it gets, need not necessarily coincide. And the same thing applies to the Fed. Bernanke wanted QE to kick-start the economy, it didn’t. He wanted it to encourage banks to lend to small business, it didn’t. He wanted large employers to invest in new products and more staff, they didn’t. Life is what happens, as John Lennon remarked, while you’re busy making other plans.

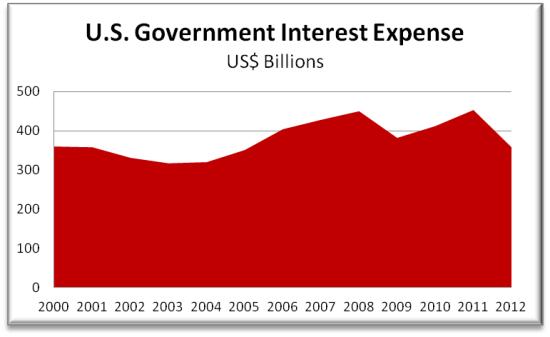

We are going to get higher interest rates. And it’s hard to overestimate just how quickly higher interest rates could blow the West’s strategy sky-high. Since 2000, the US national debt has ballooned from around $6 trillion to $16 trillion dollars. Take a look at this chart, however, which shows how the cost of servicing it has been relatively flat.

As you can see, while the amount outstanding has almost trebled, the cost rose very little between 2003 and 2007 – and hardly at all after that. Without Zirp, the West would be so far underwater, everyone would get the bends trying to come out of it.

So why must interest rates rise? Answer: because the policies being pursued will inevitably produce such a rise. Whatever one’s starting point, if half the planet owes more money than the noughts you can fit on a page, everything points to higher interest rates sooner rather than later.

But just for the hell of it, let’s start here: as the world economic depression worsens (and that is inevitable when most people can’t afford to consume) the larger investors in government debt – let’s for the sake of argument call them China – will be looking to up the income value of their holdings as they get far less income from exports…and far more restive citizens out of work needing welfare.

Further, as the debt markets realise that without economic income and political will no bond is safe, they will look for increased yields. The signs are clear on this one already. Outgoing US Treasury Secretary Tim Geithner made news last November by proposing to transfer the prerogative to raise the debt ceiling…from the Congress to the President. In a press conference soon afterwards, Obama Administration Press Secretary Jay Carney claimed that by raising the ceiling, U.S. creditors would see that “our government will meet its obligations”. As Forbes pointed out at the time, “That is taking Orwellian doublethink to new heights of absurdity”.

The truth is that, by telling the world in general that America has no intention of ever balancing its budget or limiting its accumulation of unsustainable debt, the White House and the Fed are oiling wheels of rate rise.

As time goes on, in fact, it’ll become clear that the US does need to inflate away its debt, because it doesn’t have either the will or the tools to pay it off. The United States of America is today, ironically, a retiree who just got Zirped the day after he took out a five million dollar mortgage. The retiree can use his savings for a while to pay some instalments, but when that’s gone, well….inflating is the only answer.

And as that happens – and trust in sovereign debt falls again – the cost of US debt will rise further…and then the Fed will try and inflate it down by screwing with the currency – because that can also help with exports.

Rule One of currency economics states that reducing the currency’s buying power must produce rising interest rates, as irresistible market forces look for ways for their income to keep pace with it….just as unionised workers did via their wages in the 1970s.

We should all be very clear about what happens next.

Of the $638 trillion notional value of derivatives now outstanding, 77%, are linked to interest rates. Let rates start rising, and multiple trillions of dollars of hedges will be activated, forcing every big bank on the leverage hook to, um, implode. Taxpayers will be asked, like they were four years ago, to cough up for another zillion dollar bailout. This too will cause sovereign deficits, reduce bond confidence, and force interest costs to go up. (Not to mention reducing consumer demand still further).

Back to the Present: shifts in exchange rates and rising commodity prices are already apparent. Both are potential drivers of inflation. In turn, the Fed, the Bank of Japan and the European Central Bank have all printed more money, which encourages low interest rates in the short term….but becomes inflationary quite quickly thereafter. Last year, ‘Bloomberg View’ columnist Michael Kinsley warned of “a fierce storm of inflation sometime in the next few years” that will “wipe out a big chunk of the national debt, along with the debts of individual citizens, and the savings of others.”

Revisit what I wrote a few paragraphs ago: Rule One of currency economics states that reducing the currency’s buying power must produce rising interest rates.

Of course, the currency rape/inflation/rates rise progress could just as easily begin in Europe: but it would have the same effect – thanks to the brilliant idea of having a globally connected banking system. Remember that during the original gold-standard debate under Nixon, France went its own way. As I will now try to explain, it would very likely do it this time too.

In the euro mix as in the US, we have the banks themselves: psychopathically self-serving and unpatriotic, they are not (as the Journal noted) making anywhere near enough money….and the customer scams are starting to backfire. But with customers gagging for income (and the baby-boomer bulge retiring) a bank somewhere is going to say “Stuff Zirp, I need to make more money”.

Now banks might well be unpatriotic, but in France they are guaranteed by the State. In desperation, an anti-Atlanticist Socialist French government in terror of a Greco-Spanish collapse will find itself with nowhere to go other than raising money with interest rate hikes. If you think the French wouldn’t do this, you need to get out more. And if you think the economy would be seen as more important than the banks among the infamous civil servant ENAs (graduates of the Ecole Nationale d’Administration) who really run France, then you clearly don’t know France at all.

Why do you think the Fed wanted socialist Dominique Strauss-Kahn out of the game as either head of the IMF or French President?

~~~~~~~~~~~~~~~~

I suppose King Canute ordering the waters to retreat must be high in the Top Ten all-time clichéd analogies, but nevertheless that is exactly what we’re seeing here. However, what most people get wrong in the Canute myth is where the blame lay. The king himself was wise, and only ordered the waves to go back so he could show his crawling courtiers at Goldemanne Sackes what idiots they were to believe such a thing was possible.

The belief of stubborn bureaucrats and disturbed bankers in their ability to stop the inevitable march of those very markets they themselves insist “must decide” would be the perfect King Canute analogy, were it not for the fact that we are a King Canute short of a saviour. Instead, what we have is Barack Obama, David Cameron, Angela Merkel, Francois Hollande, Mariano Rajoy and Antonis Samaras. Working for them are the superficially confident Ben Bernanke, George Osborne, Wolfgang Schäuble, Pierre Moscovici and Mario Draghi….whose only collective downside is that they’re profoundly unqualified to discern the unpleasantly useless nature of shit from all-conquering putty. This knowledge gap is what causes windows to fall out.

As always, the timescale remains an enigma. But as always, my observation is the same: the longer the self-delusion goes on, the more apocalyptic, bloody and potentially anarchic the outcome will be. Debt forgiveness on a global scale (alongside the abandonment of globalist mercantilism) is the only enduring solution available. We refuse to recognise this at our mortal peril.

Related at The Slog: Us, Them and You….it’s the ménage a trois waltz.