The Slog judges horse’s mouth against horse’s arse

The Slog judges horse’s mouth against horse’s arse

1.The BDI has slumped

The Baltic Dry Index, a measure of commodity-shipping rates, has collapsed 37% in ten trading days of 2014. It has fallen from 2277 at the end of December 2013 to 1370 today. This key indicator of global economic health is a warning signal for the global economy in 2014. Here’s why:

The Baltic Dry Index (BDI) is compiled daily by The Baltic Exchange, and measures what it costs to ship raw materials—like iron ore, steel, cement, coal and so on—around the world. The fact that the Baltic Dry Index focuses on raw materials is key to an understanding of who’s buying what in order to make stuff. Producers stop buying raw materials when they have excess inventory and when they stop infrastructure projects. When this happens, the BDI falls.

When it falls nearly 40% in such steep decline, it isn’t a sign, it’s a 4-minute warning. This chart shows how the decline is steeper and longer than previously:

It’s levelling off slightly at the moment. Keep your eyes on it. Remember: this isn’t a fluffy measure of expectations: if people don’t order the iron, they can’t make the cars.

It’s levelling off slightly at the moment. Keep your eyes on it. Remember: this isn’t a fluffy measure of expectations: if people don’t order the iron, they can’t make the cars.

2. The price of oil is rising

One reason we seem to have signed a nuclear-development ‘deal’ with Iran (in which we get to give them everything they want) is that the MoUs know just how disastrous under-supply of oil would be. At around $115-125 per barrel, the oil price would hit the world economic and financial systems like a block of concrete landing on a Sopwith Camel as it struggled to get speed up on the runway.

Yesterday, the price of oil closed above $94 a barrel for the first time in two weeks on a big drop in supplies. Benchmark U.S. crude oil for February delivery rose $1.58, or 1.7 percent, to $94.17 a barrel on the New York Mercantile Exchange, while Brent crude rose 67 cents at $106.27. Oil has risen 2.6 percent in the past two days.

The reason? US crude oil supplies fell by 7.7 million barrels last week…over four times more than analysts expected. This was the seventh consecutive decline in U.S. crude oil supplies.

The world’s natural oil supply is fixed because petroleum is naturally formed far too slowly to be replaced at the rate at which it is being extracted. A 2010 study published in the journal Energy Policy by researchers from Oxford University, predicted that demand would surpass supply by 2015. This why the US has gone fracking bonkers in recent times….but it looks like even that can’t keep up with use exceeding extrication.

3. Investors have lost faith in Hedge Funds

Investors have been bailing out of hedge funds at the fastest pace in four years during December 2013.

Some may find my view paradoxical or even counter-intuitive, but for me this issue is about the vital importance of timing.

Hedge Funds have had a terrible year. A lot of the money they’re losing will go (is going) into the stock markets direct. Some will go into bonds. The money’s going into the stock market just as the smart money is quietly getting out…whatever the continuing S&P rises suggest. As and when the market corrects, this new volume (with no hedge) will panic, and increase the size of the correction. Perhaps help it turn into a meltdown.

Or they might spot the rising Sovereign bond yields, going in to help the US raise debt. But that’s not such a good idea either…..

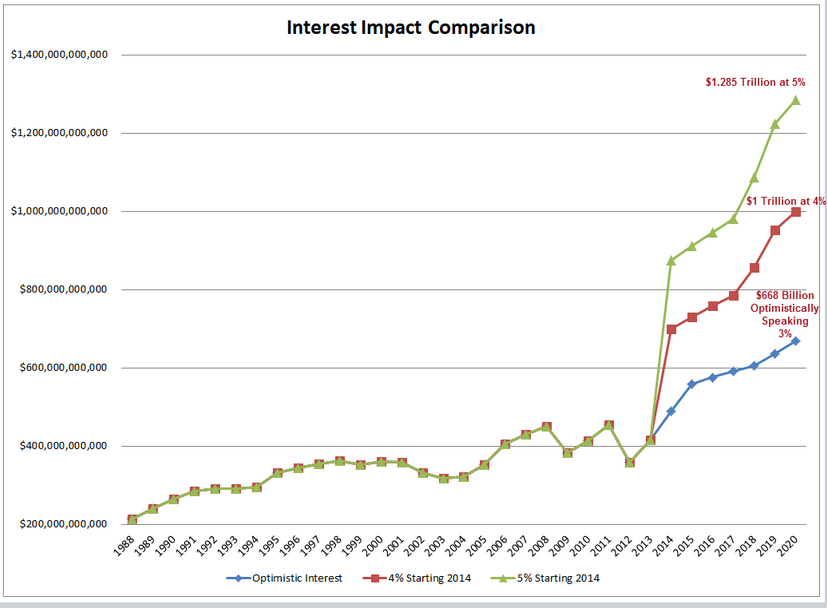

4. The rock-bottom bond yield era is ending

“I think we are in a gigantic financial asset bubble,” said respected commentator Marc Faber last week.

Bond yields bottomed out on July 25, 2012 at 1.43% on the 10-years. Things went to over 3.0%. Now they’re holding at around 2.9%. But look at the 6-month graph:

What we see here is the rise from the bottom, with failed price suppression suggesting the direction is UP. Sept-Nov’s dive has been squashed by the rise through to December, but the latest fall has been short-lived. Says Faber,

“The bubble could burst any day. I think we are very stretched.” This is what happens to US interest costs when rates go up:

5. Emerging markets aren’t equipped for the taper

The emerging “Fragile Five”markets didn’t respond well last year when a tightening of money was even hinted at by Bernanke. But as central banks tighten monetary policy for real now, we’re taking about rather more than five countries at risk.

Yesterday, the World Bank talked of a repeat of last year’s turmoil in emerging markets after Ben Bernanke, the chairman of the Federal Reserve hinted in May at plans to taper the Fed’s monthly asset purchases. If the adjustment to tapering proves “disorderly”, financial flows to developing countries could decline by as much as 80% for several months, the WB chaps.

When judged by their perceived ability to repay short-term foreign borrowings the countries particularly exposed to the fallout of tapering are South Africa, Turkey, Brazil, India, Indonesia, Hungary, Chile and Poland.

Think on this: if Bond yields continue to rise and the US can’t afford to reverse the taper, these emergent countries are going to be in for a rocky ride.

6. ClubMed ‘confidence’ is a false flag

It’s now turned out that Japan was the biggest investor in Spanish and Italian Sovereign debt bonds recently. All that guff about “confidence returning” to ClubMed has now gone away, as what Japan’s up to generally is, I suspect, designed both to prop up the EU and thus keep one of its most lucrative markets alive….with the hope in turn that the euro’s value will rise and make Europe less of a trade threat.

Is that going to happen?

Luis de Guindos appeared before the economy commission of the Spanish parliament earlier this week. He discussed the situation at CAM, one of the former Cajas which failed in mid-2011 and was taken over by Banco Sabadell at the end of that year. Guindos admitted the cost may swell to €15bn as the CAM’s assets continue to deteriorate. Disastrous loans to developers, construction projects, buildings and residential mortgages are Spain’s unique problem. It isn’t going to go away, no matter how much woffle Rajoy give us about economic growth. As I’ve been saying for two years now, the parlous state of Spanish banks has been woefully underestimated from the start.

Meanwhile, further east in Greece, time bounces happily on along with the rest of the tumbleweed, and yet still nobody seems to give a God damn that, without further radical debt relief, the Hellenics are heading for default by the end of April at the latest. As the Economist pointed out last week:

‘Greece has lost a quarter of economic output since 2007, thanks largely to the errors of its rulers and creditors alike. More than a quarter of its workers are jobless. Soup kitchens are commonplace, as are empty buildings and shops. Unit-labour costs have been reduced by cutting wages, not raising productivity. Stripping out the murky trade in fuel, and volatile tourism revenues (up in part because of turmoil in Egypt and Tunisia), Greece’s exports are falling…’

The country has been helped by a fall in yields from 40% to 8%, but (a) see the earlier remarks about the risks from tapering, and (b) budget surplus or no budget surplus, the repayment schedule set out for Athens is a farce. It’s totally unachievable, and the IMF last year – at long last – began to say so. So with the promised Christmas debt relief withdrawn once Merkel was safely back in power (I still can’t believe the extent to which the Western press simply blanked that news) where is the money coming from to stop Greece from needing another bailout…or will the Merkeschäuble move from bailout to kick out?

As long ago as last August, Wheelchair Wolfie admitted Greece will need another bailout. But discussion of the bailout v default thing has now become an Unmentionable.

Yannis Stournaras shocked most people by turning down the IMF’s offer of forming an alliance in favour of debt reconstruction (aka forgiveness) a decision so seemingly insane, it must have an ulterior motive. Quite what he expects to get in the way of constructive help from the EUnatics eludes me: A Gallup poll published last week showed how, in Greece, approval of the EU leadership stood at 60% in 2009 but plummeted to 19% last year – the lowest rating in the Union.

My view of EU officials and pols is that they are starting once again to swan about as if the crisis is abating. None of them – not even Merkel – seem to grasp the reality of knock-on effects in a globalised and financially unbalanced economy. Nothing has changed since both the European Commission and Samaras said last year (along with the IMF) that debt relief was the best approach “going forward”. It was the best solution in 2010, but it’s too late to go there now.

“It is an illusion to believe Greece could start borrowing on financial markets again next year,” the Greek parliament’s budget office said last October. But now Samaras is regularly talking of exactly that.

What are we to make of all this? My conclusion is the commonsense one: they’re all over the place, and spouting whatever rubbish comes to mind in a bid to hold back the inevitable. Two years ago, Ben Bernanke said the ClubMed crisis would have “a negligible effect on the US economy”. It was a very careful choice of words: a further spike in bond rates would sink Greece, and a disorderly Greek default would inevitably impact on US 10s. That’s the reality: which way round it happens depends on events from now on.

7. China’s silent QE fest

Much attention has been given to Japanese Abenomics (Sun headline – they’re deranged) but still very little is being written about whyTF China is piling in with its own QE bonanza. Rather than choose to use surpluses as a means of upgrading the living standards of its poverty-stricken 88%, Beijing is trying the very economic stimulation it was so holier-than-thou towards the US about two years ago.

Since 2006, the amount of money in the Chinese economy has tripled. China has little to fear from inflation at the moment: however, it is significant that the Government there has been printing more Yuan to finance billions of dollars being spent in the world’s currency markets to deflate the Yuan’s value and so keep Chinese exports cheap.

In short, this is just another stage in the China v Japan v America race to the bottom – ie, mercantile war going by another name. It can only exacerbate the trade imbalance problems that go hand in hand with adopting the globalist neoliberal model….while running the very real risk of creating all kinds of unstable bubbles along the way.

Above all, if one looks closely at the ClubMed, Chinese and Japanese moves together, we are in the desperation stage of Crash 2. If the economies involved had genuinely robust or even recovering economies, they would not be getting up to any of this malarkey.

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

We’re still on board the doomed vessel, waiting for the tipping point. We still don’t know how quickly it’s going to start, and how fast it might happen. But viewed dispassionately, the simple iceberg analogy is no longer appropriate. More accurately, the aircraft carrier Baltic Dry has slowed down, thus making an iceberg collision less deadly. But the steering has stuck. Thus it is a sitting duck for Asian submarines firing currency torpedoes, Wall Street refusing to shut the leverage scuttle-gates, and nervous bond pilots accidentally dropping bombs on their own ship.

To be fair, some of the seven sh*tstorms could cancel each other out….but not all of them. Stay tuned