Part Two of The Slog’s inside analysis of EU debt politics

Sources allege central bank directionalising fix to save Italy

Draghi & Cannata’s personal lifeboat

How Hollande was ‘arm-twisted into economic reform’

Despite an outstanding bond debt of €1.7 trillion, a frozen government, and a flatlining economy, money for debt bonds is pouring into Italy’s basket case. In this second part of a debt politics special, The Slog analyses the forces that made Draghi act, and the likely effect of the move on the sudden change in direction from Francois Hollande.

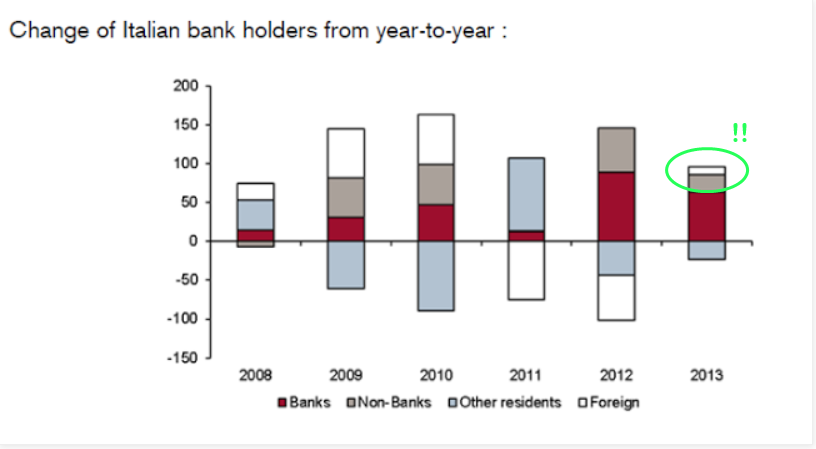

Up until a month ago, foreign holdings of Italian bonds had fallen to only a third of the total. The decline began as Italy came surging onto the debt radar in July 2011, and nervous money pulled out.What saved the Italians was its central bank buying neo-junk sovereign debt bonds from the Italian Treasury in huge amounts. This clearly couldn’t last forever, but in the midst of Beppo Grillo, Bunga-bunga and Parliamentary stalemate, it got sorted of parked on a small, spluttering back burner in a corner of the overheated kitchen.

But then last November – almost like Bernanke and his ‘taper’ – Italy’s head of debt at the Central Bank Maria Cannata called time, saying that Italian domestic banks would drastically curb their holdings of sovereign debt during 2014. As I recorded in the first part of this analysis, Italy already has the largest debt issuance in the EU. On January 6th 2014, the Treasury quietly announced that in the coming year, it’s going to issue even more debt bonds.

This truly made Italy a unique traffic accident in the eurozone. While Spain’s mess seems just as bad (in different ways, it’s worse) Madrid has announced that it will require less debt issuance this year. It also has one concrete achievement, albeit hyped: a better export performance based on lower production costs. Italy’s trade balance is far more stagnant in origin: it imports and exports a risible amount. The country is on its knees.

ECB officials (so I’m informed) met with Brussels bigwigs, and Berlin was also – despite very strained relations between the Merkeschäuble/the Bundesbank and Draghi/the ECB – brought fully into the loop.

Berlin seems to have taken the situation in its stride. If ever there was a red warning flag to sound the alarm for dirty dealing off the bottom in ClubMed, then the run-up to Christmas 2013 was it. Almost every financial commentator forecast that ClubMed States would be in trouble as interest in buying distress debt bonds waned…especially with local central bank support pulling back.

But that’s the opposite of what happened. Suddenly, big money was flowing into Spain, Italy and Ireland….and the MSM was full of bollocks about “analysts seeing the turnaround”.

Of course, there was and is no turnaround. What (it is alleged) has been put together is an EU/global central banker fix to stop the following disastrous events from tumbling into place: failed ClubMed bond sales >> spiking ClubMed bond yields >> sharks circling the Italian basket case >> Italy’s ability to honour debt in doubt >> contagion rains on Spain’s ‘recovery’ parade >> eurozone destabilised >> German voter wakes up to the Merkeschäuble electoral con >> Wall Street facing massive debt insurance Tsunami >> Asia loses key European market as consumption collapses further >> Abenomics explodes >> you don’t want to know the rest.

“Basically,” The Slog’s longstanding Brussels mole told me last weekend, “there is some kind of merry-go-round scheme, under which the central banks in one Member country buy the debt bonds of another, and the operation is disguised further by putting it under different accounting headings, and then the ECB ‘sees them right’ by printing some more money to reimburse their purchase cost.”

This is not new news…and isn’t remotely way out there and wacky: central-bank buying globally accounted for over 50% of the total demand for bonds in 2013, and as both media and markets have wised up to this, the ECB has, I know from other sources, been at this ‘disguised QE’ racket for some time.

This time, however, it seems that the scam had to be bigger, because the potential backwash was so much greater for the global economy. In my opinion, there is only one bloke with the guile, vision and contacts to pull such a thing off: Mario Draghi….and others in Europe share that view. But equally – despite Merkel’s comfortable win in the Bundesrepublik elections – Draghi had to be sensitive to the Weidemann/Bundesbank fears about German debt exposure.

It is highly possible that, at some point in this process, France (more exactly, Francois Hollande) wound up being the bait to get Berlin onside. Hold that thought.

I do not know the exact modus operandi here. The arrangement is necessarily loose and secret. But there is a further observation emanating from Madrid sources suggesting that key Wall St firms and central banks (as far afield as Tokyo) were tipped off that, if they piled in with ‘directionalising’ ClubMed bond purchases, they would be well rewarded….as of course they would be, by later quietly selling on their purchases at a profit to ‘sap’ money drawn into the apparently wonderful new world of ClubMed recovery.

As I tried to make clear in yesterday’s Part 1 of this post, this ‘scheme’ has not been put into place as a means of making Iberio-Italian debt sustainable: that simply can’t be done on any model currently acceptable to the markets.

Rather, it was put together to distract from the immediacy of Italy’s problem…with everything to play for. Greece couldn’t sink the eurozone today. But Italy and Spain would. This isn’t can-kicking: this is highly-skilled transporting of a Domesday Bomb down the road, in the hope that somewhere further along, it can be disarmed.

It’s nigh on impossible for The Slog to get hold of/strip away the disguises of the audited list of ClubMed bond purchases. But Zero Hedge pointed up the Japanese element over a week ago. I invite anyone with the forensic skills and budget required to give this a shot. I can’t prove it, but I can assert that heavy-hitters in the eurobonds market and two European capitals think there is clear evidence for it.

I will go further however, and demonstrate that Mario Draghi has a strong personal motive for “doing whatever it takes” to stop worms wriggling out of Italian cans….as they inevitably would in the event of an uncontrolled Italian meltdown. On 26th June 2013, the FT dropped this bombshell:

Basically, the story alleged (to the point of near-proof) that Draghi fiddled the Italian entry conditions for the new euro currency by making derivative trades look more solid as assets than they were. The Pink’un somehow got hold of a 29-page report by the Italian Treasury in the first half of 2012, detailing Italy’s now massive exposure to these derivatives. The report included details of the restructuring of eight derivatives contracts with foreign banks with a total notional value of €31.7bn.

The following extract from the piece was particularly outspoken – especially for the FT:

‘Mario Draghi, now head of the European Central Bank, was director-general of the Italian Treasury at the time, working with Vincenzo La Via, then head of the debt department, and Ms Cannata, then a senior official involved with debt and deficit accounting. Mr La Via left the Treasury in 2000 and returned as its director-general in May 2012 – with the backing of Mr Draghi, according to Italian officials.

An ECB spokesman declined to comment on the bank’s knowledge of Italy’s potential exposure to derivatives losses or on Mr Draghi’s role in approving derivatives contracts in the 1990s before he joined Goldman Sachs International in 2002.’

Jean-Claude Trichet (ECB boss at the time who smoothed Draghi into his succession) later vetoed an attempt by French media to get a clearer statement out of the ECB. Smoke, fire, etc etc.

Now comes another fascinating connection. The lady who heads up Italy’s debt management Quango, Maria Cannata (left) was the same Maria Cannata visited by police of the Guardia di Finanza in April 2012, and asked by them for more details of the derivatives transaction concerned – which she supplied. Ms Cannata didn’t enjoy the experience. She is also the same Maria Cannata who told the media two months ago that Italian Banks would not support Italian debt bonds at anything like the same level any more. There are rumours that Ms Cannata is nervous about some of the, um, practices involved in this.

Now comes another fascinating connection. The lady who heads up Italy’s debt management Quango, Maria Cannata (left) was the same Maria Cannata visited by police of the Guardia di Finanza in April 2012, and asked by them for more details of the derivatives transaction concerned – which she supplied. Ms Cannata didn’t enjoy the experience. She is also the same Maria Cannata who told the media two months ago that Italian Banks would not support Italian debt bonds at anything like the same level any more. There are rumours that Ms Cannata is nervous about some of the, um, practices involved in this.

Cannata joined the Italian Treasury as an analyst in 1980, and has worked her way up holding various positions, becoming ever more involved in active public debt management.

She was entrusted with the transition to the euro by the Italian Treasury. She is also a member of the EU Sub-Committee of Government Bills and Bonds Markets, of the Steering Group of the OECD Working Group on Public Debt Management, and of the Governance Group of the OECD.

So then, a network almost as good as Mario Draghi’s. At the time of the derivatives debt scam, Maria Cannata was working very closely alongside Mario Draghi (see above) as a senior official working on deficit accounting. Draghi liked and promoted her within the agency.

You could say, in fact, that Maria had as much to lose from Italian meltdown as Mario. She too has been talking Italy up of late. In an upbeat frothy pr piece in Euroweek, Cannata alleged:

That simply isn’t borne out by the facts. The first claim is contradicted by the debt structure chart I showed yesterday, and the second (as this chart supplied by US source Butch shows) is somewhat fast and loose with reality. What she says is accurate, but this is what it looks like:

That simply isn’t borne out by the facts. The first claim is contradicted by the debt structure chart I showed yesterday, and the second (as this chart supplied by US source Butch shows) is somewhat fast and loose with reality. What she says is accurate, but this is what it looks like:

Maria is a bullsh**ter up there with Mario. She has the contacts. And she too obviously realised the importance of foreign involvement when it comes to creating false confidence in Italian debt. “We are confident about a significant and growing presence of institutional foreign investors,” Cannata told Reuters in November. Why? We can only guess…and keep digging.

Maria is a bullsh**ter up there with Mario. She has the contacts. And she too obviously realised the importance of foreign involvement when it comes to creating false confidence in Italian debt. “We are confident about a significant and growing presence of institutional foreign investors,” Cannata told Reuters in November. Why? We can only guess…and keep digging.

Maria likes talking about Japan; last year, she told a journalist source of mine she expected Italy/German bond spreads to fall once Abenomics/BOJ purchasing got to Europe. That does seem to have happened: but Zoeb Sachee (the head of European government bond trading at Citi) specifically predicted, “There’s going to be a slow and protracted flow, I don’t think the asset allocation decisions are going to be made in the space of a month.’ Yet they have. The Slog’s Madrid source is equally doubtful about how likely the Japanese would’ve been to pile in without, shall we say, some persuasion. He confides, “The Japanese are incurably, even rigidly, cautious about overseas investments, especially in Europe right now.”

Most analysts as late as mid December said any Japanese inflow “could take several months at least” and was unlikely to go big on ClubMed. JP Morgan’s Carl Norrey agreed late last year: “We know from what we’ve seen before that (Japanese) targets have been mainly France, and when yields have risen they’ve got back into Germany and at times they look at the Italian market”. Again, hold that thought about France.

But Japanese money poured into Italy in three weeks. And from elsewhere. Oh so conveniently for the Mario/Maria leap into la Dolce Vita.

So anyway, why do I say “keep an eye on France? France’s debt structure is, after all, far more sound than Italy’s. The French State incontinence when it comes to spending has for certain at last landed then in potential trouble. But just as suddenly as the bond buyers switched to ClubMed, France has been struggling this year to attract buyers of its debt.

The French government debt auction last week drew the weakest demand in a decade as investors piled into Spanish and Italian securities. The yield on France’s benchmark 10-year bonds is at 2.5% now…up rapidly from a record low of 1.74% last year. After Belgium, French bonds are suddenly the worst performers among the euro region’s major issuers this year.

The MSM analysis of this switch I find, yet again, unconvincing. “France is lagging behind in the process of regaining competitiveness,” said Gareth Colesmith, a senior portfolio manager for Insight Investment Management Ltd. France is ‘lagging behind’ Spain and Italy? Are you serious?

Spain “has won praise from economists for generating record exports last year by squeezing labor costs” said another commentator, “and the efforts have been rewarded in the bond market.” Yes chum, but France isn’t carrying dozens of empty banks and fictitious property developments. And Italy hasn’t won praise from anyone.

“Italy, unlike France, has a trade surplus” said another. Italy has a trade surplus based on exporting two cigarettes and importing one.

France is in medium-term trouble – and short-term trouble if bond rates and other interest rates spike. But the uncanny coincidence of France suddenly being talked down, followed by a massive switch out of Paris into the peripheries, is counter-intuitive. In my view – and that of others with whom I have regular market contact – it smacks of directionalising.

Obviously, in a relatively size-static Sovereign bond market, there must be winners and losers. My two questions remain: why so quickly, and why in this unexpected direction?

I’m not sure the answer stops in Frankfurt and Rome. I think it also concerns Germany’s deteriorating relationship with France.

A week ago today, Francois Hollande suddenly popped up and said something important and focused. This is a first in the Hollande Presidency. But it’s what he said that concerns us here: what he said in the light of the hammering his debt bonds had taken in the previous fortnight:

President Hollande spoke about cutting public spending by €15bn this year and a further €50bn by 2017, and about his “Responsibility Pact” to reduce charges for business and cut red tape. For a Socialist President, this was a massive conversion to l’Anglo-Saxonism…largely overshadowed by florid questions about his sexual adventures.

FN leader Marine Le Pen immediately attacked the speech as “a plan for the Germanisation of France”.

Reuters confirmed that ‘Berlin has been discreetly encouraging Hollande to take similar steps since the Socialist became president in 2012’. What Reuters doesn’t tell us is, discretion was getting nowhere. Merkel was getting impatient, along with her little friend Wolfie, for the grand neoliberal plan to be extended into the heart of Socialist idleness and agricultural inefficiency. And both wanted France firmly “in the cage” after Fiskalunion.

German foreign service reactions were gushing.”Germany also took its time and had to overcome certain hurdles before it could agree on reforms of the economy and labour market that promised improvement in the economic situation,” said Foreign Minister Frank-Walter Steinmeier, a member of the German Social Democrats (SPD) and Schroeder’s former chief of staff. “What the French president presented yesterday is first and foremost courageous,” he added, describing the measures as a new direction in policy that would help not only France, but Europe to “emerge stronger from its financial crisis”.

“We really must make French exports more competitive,” said Hollande in his speech. This has been Draghi’s mantra to the EU FinMins for nearly two years. And so, the circle is complete.

It’s amazing what a bit of financial pressure can achieve, on occasions.