CORRECTIONS: THE MARKETS KNOW PERFECTLY WELL THAT THIS IS JUST THE BEGINNING

CORRECTIONS: THE MARKETS KNOW PERFECTLY WELL THAT THIS IS JUST THE BEGINNING

For those too young (or late) to realise it, The Slog as a brand name is derived from the term Bollockslog. Following last week’s end of the beginning of the end of globalist neoliberal mercantilist claptrap, you may have noticed that the bollocks has been spewing forth from the defenders of this foundation-free and entirely idiotic ‘model’ of capitalism. But we should not be deceived.

Two inalienable truths remain for critics of this economic construct to keep banging on about:

1. The world economy has been 100% dependent on sovereign debt and consumer credit for the best part of fifteen years.

2. The current system’s ability to find finance via banks and bourses is not sustainable without constant injections of taxpayer monies.

This second point is really the killer, but both are fundamental. We are being asked to believe in/support/accept or whatever a system of economic activity that works like this: 97% of electors subsidise it (by maxing credit cards, losing interest rate income, paying higher taxes, and being deprived of social services) while 3% of troughers at the top hoover up all the money for themselves.

Put succinctly: consumers have no real money with which to consume, and the private sector has no liquidity to help producers grow.

Ergo, the system grinds to a halt…very, very slowly….until an important sovereign debt is no longer sustainable, and/or borrowing rates rise, at which point, the entire deck of cards collapses.

Night and day, week in week out, two things have to be in perfect focus all the time – just to keep even the appearance of there being a show that might be on the road: QE driven liquidity, and Zirp. Stop doing either, and boom, you’re dead.

…………………………..

But you wouldn’t think that judging from the ‘élite’ output. This is from the freshly-baked IMF Report for October 2014. I’ve highlighted the bleeding obvious and the blinding illogic therein:

‘Despite setbacks, an uneven global recovery continues. Largely due to weaker-than-expected global activity in the first half of 2014, the growth forecast for the world economy has been revised downward to 3.3 percent for this year, 0.4 percentage point lower than in the April 2014 World Economic Outlook (WEO). The global growth projection for 2015 was lowered to 3.8 percent.

Downside risks have increased since the spring. Short term risks include a worsening of geopolitical tensions and a reversal of recent risk spread and volatility compression in financial markets. Medium-term risks include stagnation and low potential growth in advanced economies and a decline in potential growth in emerging markets.

Given these increased risks, raising actual and potential growth must remain a priority.’

It’s like something out of a Solzhynitsin novel about Soviet doublespeak. Why have growth targets been reduced? ‘because of weaker than expected activity’. You don’t say, Cisco? I was thinking maybe it might be down to sunspots, or perhaps a supply-chain problem in the treacle-bending sector.

And don’t you love those medium term risks? Stagnating developed markets, low potential, and declining potential. Jumping jetcars Batman, stagnating decline and an absence of potential….that’s a pretty exhaustive risk-list.

But fear not, because the Lone Ranger and Tonto have made raising potential their next stop on the DoGood trail. “How do yer think we’re gonna raise that low decline into high growth Tonno?” The faithful Indian pauses before responding to the superior White masked man. “Keemosabbe, important we make economy low in decliningness, high in growingness”. With a hi-ho Silver and ha-wayeeee.

The truth is – as nearly always – very much simpler. The people out there doing the buying, selling, directionalising and cash-cow milking (but not a lot of wheel-oiling on the whole) know the game’s up, and the only thing on their minds right now is how to keep a close eye on the vintage Krug glass.

There is no test in history that can match the Krug Test. It works like this: we’re all on a big ship, a ship so big and unwieldy because it has been built to go at very high speeds but not to avoid big lumps of hard stuff in its path. The trick is to constantly trough 24/7 at the goodies table, while always having a beady eye on the Krug glass.

When the glass shivers a little, and spills a minute drop of the amber nectar onto the caviar-stained tablecloth, we’ve hit the iceberg. So this is the time to smile at the glass, drink its contents, and every so casually retreat from the dining room to the comfort of that First Class Cabin, open the safe, put all the jewellery in a carpet-bag, and load the Colt 45 to the brim with lead.

The next stage will involve a great deal of volatility, but for your personal chances of survival to remain in double figures, the chief requirement is the bold act of jumping up to the nearest lifeboat, putting a gun to the steward’s head and shouting (with a degree of firmness) “F**k the women and children, lower this sucker into the sea before the SS Leviathan drags us under”.

That such volatility lies ahead is obvious to those running the show, and luckily we can measure this using the Vix, or volatility index….more precisely, expectations of what the Vix will itself show going forward.

Last week’s Vix of itself was small compared to 2008. But the forward expectation was higher than anything ever recorded before. Put simply, this means that the vast majority of people not only think that much worse shit lies ahead: they think that nobody can see any fat ladies singing, and for that matter we don’t even know there’s a fat lady with a good voice on the ship.

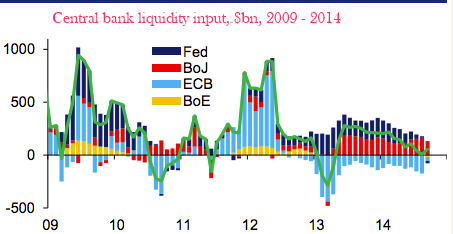

Equally simple to explain is why they think that way. The chart below shows the degree to which Point 2 at the start of this piece is incontrovertibly correct:

For me, there are two startling colours in the above: the the Bank of England, and and the ECB. For what they tell us is that at the end of 2013, the two big Europe-based central banks of the Pound and Euro gave up on liquidity injection – ie, QE.

For me, there are two startling colours in the above: the the Bank of England, and and the ECB. For what they tell us is that at the end of 2013, the two big Europe-based central banks of the Pound and Euro gave up on liquidity injection – ie, QE.

Now, we already knew that about the Dollar’s Fed – and that’s confirmed by the tailoff in navy blue. But what we can now do is see how the markets have reacted over time, leading up to last week. The bottom line on this in hard cash terms is that just stopping a market rout costs the public purse some $800 billion a year.

In an astonishingly bonkers piece for the Daily Telegraph two days ago, Ambrose Evans-Pritchard opined that such a permanent QE position might be inevitable. He just didn’t say how on earth that could ever be either possibly or desirable.

Abe san in Tokyo, of course, thinks it’s just a matter of scale, because he is mad. But the crucial point to take away from this analysis I would summarise as follows. If the cost of keeping the circus alive costs “the West” not far shy of a trillion bucks a year – and the West is already neck-deep in further trillions of debt – that sum is unaffordable. But if you take away the stimulant, the patient goes into a coma.

This is known among the elevated circles in which I operate as the Lifeboat or Drown Event.

………………………………..

The human misery that has been inflicted upon entirely innocent electorates in order to prop up this ridiculous cross between sham and scam is off the scale of pernicious insanity, but whatever the smug cynics believe, push is now coming to shove.

A desperate jobless father entered the tax office in Rhodes holding in his arms his 18-month-old baby earlier this week. “Take it,” he told the stunned tax officers “I cannot feed it anymore.” The father discovered that the tax office had confiscated €300 from his bank, which meant he was skint.

Not only did he find himself in that position as a result of corrupt, spineless politicians who over-borrowed from rapacious lenders; he was also in that position because a trident of greed, Washington and Brussels (egged on by Berlin) force-fed the Greeks an austerity plan certain to depress consumption in a capitalist system that could only function in the first place through fake money aka credit.

Now I am not saying here that a starving populace will make any of these dangerous lunatics change direction. To think that really would be to adopt a naivety flying in the face of all the empirical evidence. No: what is going to happen now is that those wannabe survivors without guns to force the lifeboat issue will try and buy one….in a situation where guns are scarce, and the stern is rising out of the water.

And that’s the point at which the steerage passengers will decide enough is enough….unless forcibly dissuaded from such a conclusion.

………………………………..

Logically, I think we are looking at another, this time more concerted, correction in stock markets fairly imminently. Then two options remain, each delivering its own likelihoods:

OPTION 1: THE SHIP IS DOOMED, EVERY MAN FOR HIS OWN LIFEBOAT

* Collapse of the entire fabric of banking, investment, and economic activity.

* Anarchy, chaos, revolution, widespread violence

* Breakdown of vital services allowing pandemics to spread

* Resultant huge cull in the human population as a result of civil strife, nuclear exchanges and disease.

OPTION 2: THE SHIP IS SALVAGEABLE, WE MUST LIMP TO THE NEAREST PORT

* Growing awareness of the markets’ doom

* Exacerbation of that with a rapidly deteriorating eurozone crisis involving one or more of failing banks, lost confidence in the ECB, Bankfurt rebellion against the single currency, Italian default and French truculence

* Money-printing on a massive scale

* Lurch to the hard-Right in the face of divided and muddled liberal Parties

* Emergency Powers being extended beyond ‘anti-terrorism’ laws

* It all depends, hard to tell etc etc etc.

My money is on the second option, which might be both a good and a bad thing. Certainly, in that eventuality the outcome will depend entirely on whether the thinking minority can outgun the thoughtless élites, and thus get the brainless onside against those élites. David Cameron says I am now a non-violent extremist, and so obviously I would want the whole thing managed without violence. Whether it will be or not is an entirely different matter.

However, I thought I’d end this essay with an extract from an email sent to a Greek friend earlier today: