CRASH2: Reality intervenes, so time for a bigger dose of unreality

I’ve been blogging about the gold-dump syndrome for over six years, and the phenomenon rarely changes in either form or aperture.

Last week’s fears about falling oil prices saw a medium-strength rally in the gold-tracker sector alongside stock market jitters around the globe. Greece saw 20% wiped off its bourse value, and mid-eastern markets have been bloody. In short, a brief return to sanity – aka, the fundamentals.

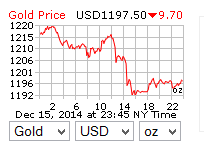

Yesterday the Middle East markets had a terrible day, oil fell further, the Rouble dropped again, and European markets fell an average 2%. This is what happened within 30 minutes of the NYSE opening:

For gold to do that in the current news context is well beyond counter-intuitive – it’s a manipulative intervention, designed yet again to keep market sentiment about the Escape to Gold nervous to negative. It’s also a nonsense in basic marketing terms:

For gold to do that in the current news context is well beyond counter-intuitive – it’s a manipulative intervention, designed yet again to keep market sentiment about the Escape to Gold nervous to negative. It’s also a nonsense in basic marketing terms:

Be in no doubt about this: The supply of newly-mined physical was down 7% in Q3 2014, but demand was up.

The game being played now in this last Act of Crash2 is poker – and the players are gambling that their spin and directionalising can win on two dimensions: who has the most money – central bankers (led by the Fed) or the markets? And which is strongest – the selling power of the reserves, or the buying power of panic?

The answer to the first question is a fairly straightforward one: the sovereign bankers have more access to large dumping quantities, but the markets have far more money.

As to the second, well…it depends, but history tells us that panic always has the last laugh….if mirth is an appropriate emotion here. And if sovereign CBs dump too much now, but a market-driven breakout overwhelms them….ooops….bankers in new doo-doo shocker.

What this all adds up to is that sovereign gold holders are effectively in the Alamo: sooner or later, they’ll be overwhelmed by Santa Ana market sentiment beyond the walls. But the market for what exactly? That’s the key question.

Many pundits continue to rubbish the exchange traded fund (ETF) tracker investment as not really backed by gold at all. I think they’re right – I’m sure it isn’t – but is that relevant? Unless the tracking data itself is bent, the ETF is still monitoring the price of the real stuff in the mainstream bullion sector. Now as anyone capable of ringing a bullion dealer will tell you, demand for bullion has never been higher: in 2014’s third quarter: investment demand posted a 6% increase, reaching 204t, Central Banks added a further 92.8t to their coffers. And supply was down 7% in Q3.

Exactly how the price is being damped down (when physical demand is high) remains something of a mystery….I’d imagine several tactics are in play. But whether it’s happening or not, we can see from the above data that investors are still buying twice as much as the CBs…who, in buying themselves, are piggy in the middle of a tug-o’-war between two rugger sides: if they buy too much, the price rallies. And ETFs will reflect that. In fact, at a certain price one has to assume that there will be a coordinated buying spree by sovereign banks. They hope to put off a price breakout until they’ve scoffed their fill, but again it really doesn’t matter: the ETFs will reflect this, and within micro-seconds of the move taking place, there’ll be an investor stampede.

The three risks with ETFs are: one, a revelation proving that there’s no physical backup; two, sovereigns banning private trading in physical gold; and four, a Libor-rate style conspiracy to falsify ETF valuations. They’re still huge risks….but timing is everything.

I’m convinced a gold rush is coming; but when, or at what price, or what the size of the window might be….as usual, nobody knows.

Last night at The Slog: The Diary of Farquinelle Warwick-Hunte