Springtime for Greece & Democracy, Winter for Brussels & Globalism?

Although it may have passed 95% of humanity by, yesterday – 11th June 2015 – was a turning point in the silent war between neoliberal control and citizen fightback. The signs were relatively small, but I think telling.

Bond yields began climbing inexorably across the world, suggesting that Bill Gross is still right on the money when it’s big enough. Yields, prices, rates whatever: the important thing here is that – as I’ve always insisted it must – the cost of borrowing is going up. There is bound to be contagion from this: equally, while the ECB’s Mario Draghi will be able to claim that he has “beaten” deflation, when rates rise along with inflation it becomes a Debt Race between inflating away the debt before the cost of borrowing it results in bankruptcy. The sheer size of US, UK and eurozone debt means, if my maths are even vaguely right, that without manipulative action the central banks and their associated sovereigns will lose the race.

The only way to park the debt somewhere ‘safe’ (as if it were a barrel of Chernobyl-irradiated anthrax) is to stick it in the liabilities of a central bank and forget about it. But somebody still has to make the repayments – this is money borrowed, not money lent and lost – and the only way to do that is by direct money-printing: hyperinflation then follows….see the Slogpost from two days ago. But even then, wait just a fraction too long before hitting the print button, and the debt begins to climb so fast, only printing at close to the speed of light can catch it. The game – along with the mammories – is at that point, effectively, up.

This leaves both borrower and lender in a tricky spot: the US has the nuclear blackmail debt cancellation card, while the Chinese et al have a choice between writing it all off to experience, or calling the blackmail to see if it’s bluff.

But here’s where it gets especially interesting: US Fed data released in April this year showed that Japan now owns the most US debt – $1.2244 trillion worth of U.S. government securities versus $1.2237 trillion respectively. And both countries have been selling it like billy-o….another factor in the normalisation of bond rates and yields. Here we have a BoJ allegedly buying everything from hari-kiri futures to alchemy bonds…but unloading its US position. The only reason it has overtaken Beijing is that the Chinese are selling it even more quickly.

Between them, however, Japan and China still own under 14% of the debt. There is then the ‘hostile oil belt’ – Ecuador, Venezuela, Iran, Iraq, Libya and one or two others – who own perhaps 10% at most. The point at which the US gets into deep water is when all of them decide to sell at the same time. Only last October, Forbes postulated that this possibility was “extremely unlikely in the foreseeable future”. It’s beginning to look like the future is here.

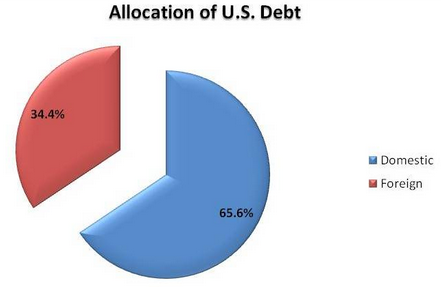

But it gets much worse than this. This chart shows the domestic/foreign split in US debt ownership:

Roughly two-thirds of the $18 trillion owed by Washington belongs to the citizens – or rather, bodies allegedly answerable to them. Social Security owns about 16% of the debt, followed by other ‘federal government entities’ (13%), and then the good old US Fed itself (12%). Quite what happens to those institutions when America defaults is not clear. But asking the Fed to buy 88% of the US debt in double-quick time is not the sort of thing for which Janet Yellen is renowned. And equally, you wouldn’t want your social security or federal pension invested in a building everyone was clambering to leave at the same time…when in the next door building, a printing press was rendering your annuity worthless.

So the US is in something of a pickle, and this isn’t being helped by yesterday’s second significant event: the IMF’s Christine Lagarde stalking out of the Greek debt ‘negotiations’ in the context of the gathering power of the Asia Investment Bank (AIIB).

La Lowgrade is under a lot of pressure from her Board and paymasters at the minute, and it’s beginning to show. Chrissy’s petulant flounce – accompanied by the usual “Greece must stop gambling” codswallop – isn’t going to solve anything. But it is nevertheless a measure of the cloud-cuckooland in which some Syriza bigwigs live that her exit didn’t stop them from once again asserting they were “confident a deal will be reached next Thursday” – that is, June 18th.

I must have my bad eye to the telescope on this one, because I see no signal of that at all. What I do perceive, however, is an increasingly jumpy America…and some risible articles designed to calm the nerves. The funniest of these was in the Wall Street Journal yesterday, headlined, ‘Brighter Economy Speeds Flight From Government Bonds’ and sub-headed ‘Selloff sends yields in U.S., Germany, Japan to 2015 highs as investors move away from safety of debt’. Oh dear.

Ambrose Evan-Elpus was infinitely more realistic in his well-document Torygraph piece of yesterday afternoon, which had some powerful sharp-end movers suggesting that Murdoch’s journal was talking cobblers. AEP headlined, ‘Bond crash across the world as deflation trade goes horribly wrong‘: his analysis was compelling.

This morning, Ambrose returns to the Greek Debt marathon, observing that ‘…..Syriza and Europe’s creditor powers are no closer to a deal as bankruptcy looms. The Greek interior ministry has ordered regional governors and mayors to transfer all cash reserves to the central bank as an emergency measure.’ The man most reviled by Poles Donald Tusk pomped, “There is no more time for gambling. The day is coming, I’m afraid, that someone says that the game is over…There are major differences between us in most key areas. There has been no progress in narrowing these differences”. In fact, Don lad – as I’ve said all along – there never has been and there never will be. It’s down to penalties now…..and the EU faces much bigger ones than the Greeks.

If Syriza stands firm, it will effectively win the most important result of all: successful resistance that forces the bully-boys to face the reality of “when you can’t repay a gigantic debt to the bank, it’s the bank’s problem not yours”. That in turn will bring on disobedience contagion…and bring down the EU.

The third event came out of a suddenly-appearing patch of blue sky in left field. It seems that Rupert Murdoch will be stepping down as CEO of Newscorp. Most of the MSM coverage today talks of a ‘fudged’ succession between the two sons James and Lachlan. For myself, I am far more intrigued by the rumour sweeping New York last night that Murdoch is distancing himself from Newscorp in order to prepare for some very heavy legal charges that might otherwise taint the company.

There are many ways one can envisage the ramifications of these three events. As a Brit, however, I see four insoluble problems heading in the direction of Cameron, Osborne, Hunt and Johnson. First, the Chancellor and his boss might as well tear up their ‘strategy’, because normalising bond rates mean that the UK’s debt bomb is about to have its fuse lit. Second, increasing bond yields and AIIB success put the Special Relationship in the Too Difficult to Solve file. Third, increasing chaos in the EU – brought on by bond spikes and Greek defiance – mean the secession advantage has now switched to the Out team. And finally, if the issues Murdoch faces are what I suspect they might be, then Jeremy H**t and Boris Johnson might in turn find themselves in a somewhat uncomfortable frame. Let’s just say that their careers might go from Money for Old Rope to Money from Old Roop. Rebekah Brooks is urgently scanning those countries lacking an extradition treaty with the UK. Perhaps she and Piers Morgan will live there happily ever after.

Have a jolly weekend.

Related at The Slog: Two jolly ho-ho-ho-hostages to fortune in clampdown fiasco