Santander boss Botin….reasons to be cheerful?

Santander boss Botin….reasons to be cheerful?

Another day of the world’s stock markets largely in the red yesterday has been followed overnight by the Chinese SSE Composite dropping over 2%, and the Hang Seng diving 3.3%. Meanwhile, South American tigers continue to sink under the weight of US Fed alleged tapering….and now Yellen yo-yoing on rate rises. Finally, the recent Spanish elections show once more that the country is in serious danger of becoming a sovereign basket case. All these events will impact directly on one bank more than most. The Slog investigates whether Santander’s ebullience is really justified.

News soundbites like ‘Ana Botin Bullish on Brazil and Santander’ always for me come under the heading of “You would say that”.Lest we forget, this is the lady who needed to borrow $7.5bn in new capital within seconds of becoming CEO. That’s only a billion less than the toxic nuclear reservoir formerly known as Deutsche Bank had to raise. Ooo-er.

The Bank has struck me for years as odd, secretive and lopsided in all kinds of ways: sort of doing that swan thing of apparently gliding swiftly across a millpond, while the brain behind those little eyes knows that a waterfall lies ahead, and the feet are already treading water.

Gung-ho analysts in recent days have designated Banco Santander SA a buy. I beg to differ.

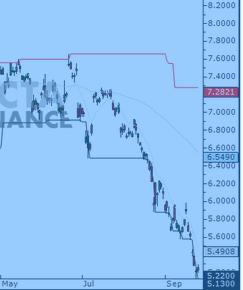

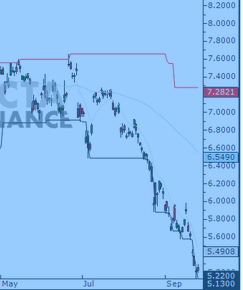

Santander has now failed two stress tests in a row. Its share price has been heading south for much of this year….and its latest phase (below left) looks like a cliff-fall.

Santander Consumer USA Holdings Inc. (NYSE:SC) has lost 2.16% during the past week and dropped 5.87% in the last 4 weeks. Yesterday it lost 1.72%. Am I the only person seeing all this as a disturbing acceleration?

Santander Consumer USA Holdings Inc. (NYSE:SC) has lost 2.16% during the past week and dropped 5.87% in the last 4 weeks. Yesterday it lost 1.72%. Am I the only person seeing all this as a disturbing acceleration?

While the pr spin the bank puts out is never less than upbeat and expansionist, buy/sell ratings analysts have been at loggerheads about whether it’s a ‘buy because it’s too cheap’ stock, or ‘sell because it’s going down the tubes’. It’s all “yes-and-no”. For example, shares of Banco Santander Chile get a Buy-Sell rating of 2.67 on a 1 to 5 scale; while based on a -1 to 1 scale, the sentiment score for Banco Santander Chile based on news since mid 2015 yields a score of 0. It all looks ‘slap bang down the safe middle’, but in reality it isn’t: it’s “we don’t know”.

An important (and unique) core of the bank is of course its Spanish homeland and South American dimension. Last April,

Banco Santander´s earnings jumped 32% in Q1 2015, after it recorded improvements in Brazil and Spain. But that was before Yellen’s Fed began to sound bullish on rates: if new family Empress Ana Botin is bullish on Brazil today, it’s time she paid a visit to Specsavers. Banco Santander Brasil’s share price has fallen from 15.4 Real to 12.5 in the last 25 days.

Moody’s yesterday downgraded Santander in struggling Puerto Rico. The island’s continuing economic contraction and fiscal crisis could lead to deteriorating asset quality at the island’s banks it said….Santander’s consolidated non-performing assets ‘are already extremely high relative to their total gross loans and other real estate owned – currently 10.3%’. And on that basis, the Moody Blues downgraded Banco Santander Puerto Rico from Baa2 stable to BCA ba3.

At Bloomberg’s analysis service yesterday, one found this re Santander SA the Group company: ‘No earnings announcements are currently available for BANCO SANTANDER SA’, which I thought odd; but on its own admission, the bank is heavily dependent on the business heartlands, none of which are in good shape. Front-foot and positive as ever, it has been letting leaks float out there that it is ‘aiming to bring its U.K. and U.S. investment banking businesses up to the same strength as Brazil or Spain’ – a clear case to my mind of sounding ambitious and wanting to be designated a ‘buy’ stock.

More accurately in commercial terms, Botin is trying to broaden by territory and diversify by sector because the outlook for Iberiphone non-investment banking is bleak. But for a bank with relatively little pedigree in Anglo-Saxon investment sectors, that looks like an uphill climb.A highly placed UK investment source told me late last week, for instance, that Santander’s British operation “has safety ringfencing that just isn’t up to it given what’s coming down the road.

Given the apparent (albeit unconvincing) determination of Janet Yellen to raise rates ‘this year at some point’, I think it is fair game to have concerns about a go-for-it bank firmly attached to a region that will suffer more than most from the US Fed’s down-the-rabbit-hole view of life. Ana Botin is in the middle of a medium-term shake-out designed to give Santander a more solid footing. I have a hunch that short-term reality will intervene to scupper her plans. If so, it will be messy…and very probably a domino-pusher.

We shall see.

Santander boss Botin….reasons to be cheerful?

Santander boss Botin….reasons to be cheerful? Santander Consumer USA Holdings Inc. (NYSE:SC) has lost 2.16% during the past week and dropped 5.87% in the last 4 weeks. Yesterday it lost 1.72%. Am I the only person seeing all this as a disturbing acceleration?

Santander Consumer USA Holdings Inc. (NYSE:SC) has lost 2.16% during the past week and dropped 5.87% in the last 4 weeks. Yesterday it lost 1.72%. Am I the only person seeing all this as a disturbing acceleration?