IMF says World faces crisis and Brexit will make no difference. Everyone else goes lalalalalalalalah

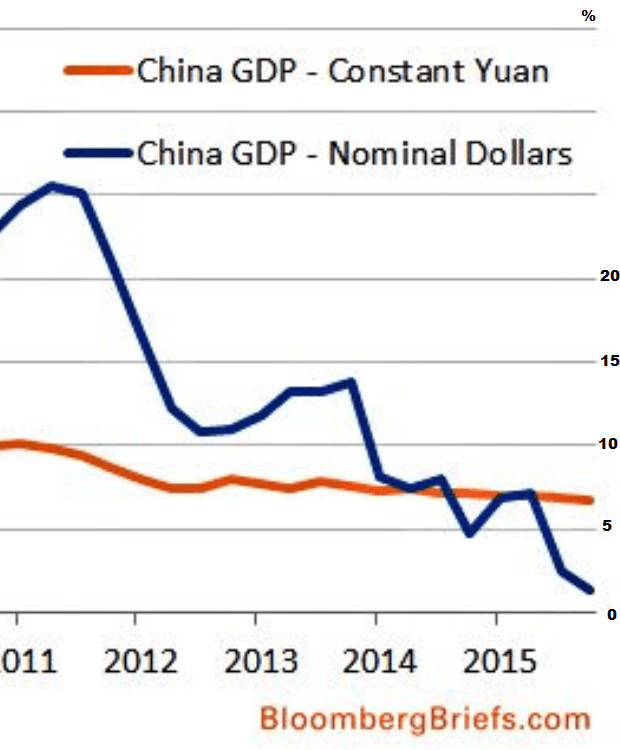

In honour of the arrival in Shanghai of Gobbledegook20 overnight, the People’s Bank of China turned another index rout into ‘profit’. Which is fine, except that Beijing is burning its reserves at an alarming rate, and the signs that it can move quickly back into growth “once the storm has passed” are getting weaker. Here’s one chart I can guarantee won’t be getting top billing at any of the G20 sessions:

I

The nominal dollar measure shows that when one replaces a falsely undervalued Yuan to assess value growth with a floating dollar unadjusted for inflation, the 2.5 year contraction in China is far steeper than anyone suggests…and it is rapidly heading for zero. It sort of blows the ‘China carefully adjusting to a more services based economy’ myth apart – a hypothesis which I remain unable to believe, as nobody seems able to tell me what these services are, and who’s going to buy them.

The same is true of Japan’s debt – the biggest on the planet cf gdp – and why anyone would pay the BoJ for the privilege of lending to a bankrupt with no job.

And now, I’m afraid, some of this EU member gdp and jobs data is beginning to stretch credulity. Here in France, the ‘news’ is that more people found jobs in January, and the economy ‘is expanding’. This is flatly denied by everything one sees, and everyone in manufacturing, retailing and construction with whom I converse.

Every last concern I know is way below target…and the falling shop prices I see every day are reflected in the latest deflation figures. So the economy’s about to take off, but, um, deflation is getting worse.

Last Autumn, Wolfie Schäuble was mouthing mendacities about Spain turning the corner: their deflation numbers this morning are twice what was anticipated, so one can only assume that round the corner there was a whopping, open manhole.

Some of you, in turn, may have spotted a Twitter swarm of Italian optimists in recent days. I’ve counted five so far….I don’t follow any of them, and yet there they are, every day, gibbering on about how the Greeks and the Brits have f***ed everything when it was all going so well before they messed up. ‘Italy’ tweeted one of these monkeys yesterday, ‘is on a sustainable road to prosperity’ – a verdict sillier yet than finding Rebekah Brooks innocent of phone hacking.

G20 or not, the EU is involved in a tooth-and-claw fight for survival, and in that situation nothing is sacred: Juncker admits that when solids hit fans “lying is the only option”. Every bad economic sign encourages rebellion, and with Brexit rebellion high on the agenda, no punches are being pulled in a bid to pretend that the UK is better off in, and doomed if it leaves.

Abe Lincoln was right in 1852, but he’d be wrong today: if you put together time-starved acceptors and a non-stop media torrent, you can very easily fool (and scare) all the people all the time. Since the Referendum date was announced last weekend, media terrorism has been at maximum volume.

“The bigger the lie, the more effective it will be,” Hermann Goering once infamously remarked, and there is no lie bigger than assertive propaganda thriving on fear to create more fear. But it’s everywhere apparent on the Brexit issue – in Establishment media, in banking firm notes to clients, and in the pro-EU Guardian and BBC. On Bloomberg yesterday, three City talking heads in London were plied with donkey-drop questions from Boombust HQ in New York, and their replies were beyond blinkered: it was ‘obvious’ to all three that the fall in Sterling reflected (quote) “the overwhelming reality that Britain simply would not survive outside the EU”. It was also obvious to me that they didn’t want to talk about who laid the eggs creating all the Stayers turning chicken; the thought that both Government and media were working 24/7 to create a self-fulfilling prophecy never got on the agenda. It really was creepy to watch….but then, no creepier than the Brussels-am-Berlin PR lies positioning all the blame for the Greek marathon on the shoulders of ordinary citizens there.

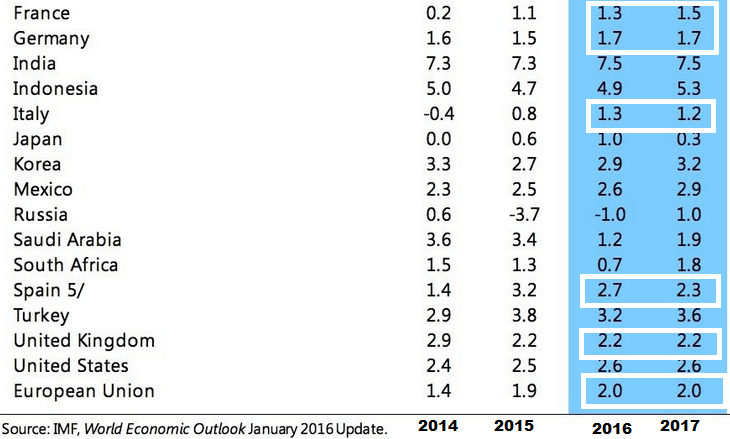

So the message for the time being is to show we boneheaded Brits how well Europe is doing. Four years ago, it was to show Greece recovering: of the 23 Greek economic forecasts put out by the IMF since that time, every last one has been proved ludicrously optimistic. This time, however, their outlook going into the G20 is just a tad off message:

The usual level of finger-in-the-air optimism is there…the data on Spain, for example, already looks wobbly – even if one accepts the 2015 number, which was without question heavily massaged to make Wolfie’s case. But otherwise, all the EU major players are predicted to do worse than the UK. Even then, if you take the gdps of those major players and still get to 2% growth for the EU as a whole, then the growth required in ClubMed and the other peripherals to get there represents sheer fantasy.

In short (and the IMF has factored this in) Fifi Lagarde’s view is that the ‘post-Brexit doom for the UK’ scenario is tosh. Interesting, that….and probably inadvertant. To be fair, the IMF is trying to instill a sense of urgency into the G20 (Lagarde is, rightly for once, more bearish than most about the global outlook) but the last thing the Chinese, Eunatics or Yanks want is any panic that might make the markets get more jitters.

“Talking about further stimulus just distracts from the real tasks at hand,” Germany’s Minister of Finance Wolfgang Schäuble said this morning, rebuffing a recommendation from Fifi that the G20 should start planning now for a coordinated stimulus program. Arriving as he does fresh from the outstanding success of his ClubMed austerity Blitzkrieg, you can rest assured that Wilfie’s views will get a warm reception. The Chinese, for example, are still saying it’s all about services balance, and US Treasury Secretary Jack Lew reitered his belief that China has “the tools to accomplish its economic transition”. He just didn’t say what they were, or why the transition was either necessary or desirable.

The EU leaders themselves are emitting a sense of Swan-like calm, urged on (I’m told) by Osborne to keep stressing how great things are in the basket case, and how great the dangers of Brexit. Using the sort of condescension only French politicians can achieve, Michel Sapin said it was best for the UK to remain in the European Union, but he expected the British people would make the “right decision” on June 23.