As the German banking crisis spreads to Commerzbank, the seemingly unstoppable demise of Deutsche may yet drag in a US White Knight…as is being suggested in Italy. But Spain is in limbo, China’s debt is getting out of control, Japan is at a dead end, and the VIX index is spelling selloff on the NYSE as never before. Catalysts produce crises, and crises lead to crashes. We’re entering Phase IV in the process: that brief time when money can be made from the negligence of overf-confident investors.

As the German banking crisis spreads to Commerzbank, the seemingly unstoppable demise of Deutsche may yet drag in a US White Knight…as is being suggested in Italy. But Spain is in limbo, China’s debt is getting out of control, Japan is at a dead end, and the VIX index is spelling selloff on the NYSE as never before. Catalysts produce crises, and crises lead to crashes. We’re entering Phase IV in the process: that brief time when money can be made from the negligence of overf-confident investors.

Describing the Chinese economy as ‘a slow-motion car crash’ in The Times, Sky’s Ed Conway adds ‘The yuan today joins the elite club of currencies, but that can’t hide the escalating debt crisis’.

He’s right. In turn, all the Davros drivel of last February about China diversifying into a services economy (we just never found out what the services were) and not affecting the West anyway (so we aren’t really global at all?) couldn’t hide the glaring reality that (a) the Government had banned selling in several sectors and (b) the PBOC was buying stocks directly if they looked wobbly.

This Sunday, the people of Hungary will go to the polls, where citizens can vote Yes or No to acceptance of EU migrancy quotas. Every survey there suggests there will be an overwhelming vote of No.

This is another step in the move among peripheral Eastern EU countries to reject diktats from Brussels, and will – I’m sure – be followed by similar reactions among Hungary’s neighbours. The migrant policy driven enthusiastically by Merkel is in tatters, and both Hungary and Poland have already made clear their resistance to taking the euro.

That begs the question, “what price the euro now?” Three issues are immediately pertinent to this issue: the German banking system, the Italian banking system, and the political standoff in Spain.

This morning, Deutsche Bank shares are under £10 in the City for the first time, having fallen 7% yesterday. With ten Hedge Funds having decided to row away from The Bismarck, its Lehman moment is arriving….and as Lehman discovered, weekends with bank holidays can either save or sink. The shares were down a further 4.4% at midday CET.

Commerzbank is also clearly in trouble, having dropped 6% this morning so far. Rather than engaging in denial, the CB management have issued plans to restructure and reduce headcount forthwith.

There were rumours in Brussels this morning that a white knight Bank is being groomed to take over Deutsche, and that Mario Draghi is behind it. These remain unconfirmed.

Nevertheless, this has already been floated as the best route for Italian banks…

With Prime Minister Renzi already under the cosh about the Italian economy – and the parlous state of at least three banks – two days ago senior bankers there were openly favouring a Jamie Damon rescue plan that would make use of JP Morgan’s enormous balance sheet.

Last July, J.P. Morgan led a plan to rescue Monte dei Paschi – which needs to offload €25billion in bad loans after talking to high-level Italian government officials. It is also among the lenders pitching to help Italy’s largest bank, UniCredit SpA, drum up at least €8 billion ($8.9 billion) of capital. But shareholders in Paschi are truculent about and wary of the deal – hardly surprising given further monies ploughed in have gone, and the bank’s share value has halved this year.

Today, it was looking like back to Square One…..

….and since the first round of elections in December 2015, Spain has been in exactly that place.

The election gave Mariano Rajoy’s right wing Troika puppets the most seats, but no absolute majority, following Ciudadanos and Podemos gains.

Efforts to forge a coalition failed, and a repeat election in June produced the same deadlock.

To make things worse, The Socialist party (PSOE) is having a Corbyn Labour moment, with seven senior shadow Cabinet members resigning two days ago in an attempt to oust the popularly elected Pedro Sanchez, a purist who flatly refuses to join a Coalition with the Rajoy Conservatives.

And of course, the regional independence movement remain a further factor acting in diametric opposition to the Brussels colonialists.

In short, both the European Union and the euro itself are staring vapourisation in the face. American banks might get involved on at least two fronts, the ezone economy hasn’t responded to Draghi’s QE splurge (just fancy that), and all the reassuring fog about China’s inner strength is disappearing in the early Autumn sunlight.

This begins to make the world’s bourses – as I’ve been banging on about since 2013 – look insanely overvalued, pumped up as they have been by QE and Zirp. Having tried every lunacy in existence including Nirp, Japan knows not where to go next.

But what are traders in the US making of it all?

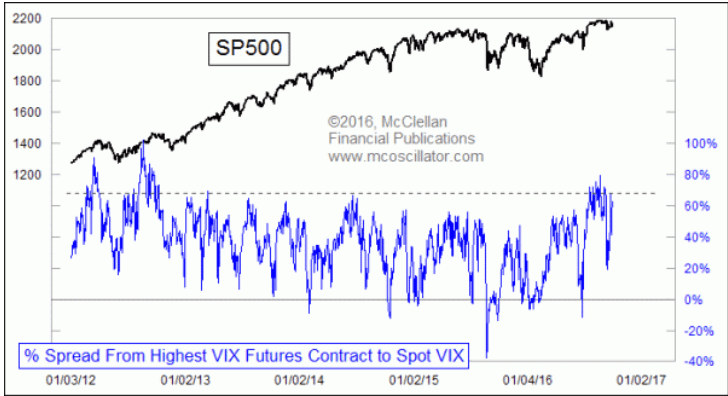

This chart from Tom McClellen posting at NTMarkets this morning shows just how ominous market expectations of volativity are:

The volativity index (VIX) is a glorified one-armed bandit via which speculators are able to bet on the degree of future volatility they expect. But what this comparison of the Vix with the S&P 500 actual performance shows is that – whereas in 2012 and 2o13 fears about volatility did keep stock prices at a sane level of real uncertainty, the rise in the Vix since the turn of the year is being ignored by Bulls.

In a nutshell, it says the current Goforits are being idiotically rash. They’re Bulls emitting Bullshit.

A selloff in these conditions is a good 20-1 bet. And that’s the bet I’m going to take. What you do, of course, should not be based on what I do, as I’m just an amateur who doesn’t know what day it is and spends half his time intoxicated.

Enjoy the weekend.