The markets will always decide. The problem with that reality, however, is that markets are just collections of technology, directionalisers, cheats and run of the mill neurotics with issues. They screw up. Everywhere one looks on the bourses at the moment, frontal lobe syndrome rules, and the right sub-arachnoid hemisphere is in control. It’s time to restate the case for gold.

The markets will always decide. The problem with that reality, however, is that markets are just collections of technology, directionalisers, cheats and run of the mill neurotics with issues. They screw up. Everywhere one looks on the bourses at the moment, frontal lobe syndrome rules, and the right sub-arachnoid hemisphere is in control. It’s time to restate the case for gold.

There’s a madness in the air at the moment. Like the smell of bacon on a winter’s morning, it is unmistakeably tempting, and the cause of salivating expectation. But stuffing your face with bacon every day is bad for a person. Bacon is a false God. Also it’s not kosher.

As usual over the last five or six working days, I’ve been Channel surfing, and generally ringing round to gauge reactions to probably the most surreal year of my lifetime. Doing so has confirmed my sense of something beyond bullish taking place. What we’re seeing now isn’t a bull run: it’s a drove of pigs jostling with each other in their haste to get to the cliff edge, where their ability to fly will become apparent to all.

Except pigs can’t fly. It’s one of many reasons why bacon is never in short supply.

Across the main business news programmes and channels at the moment, everyone is locked into New Paradigm gabble. I’ve joked before about the way the presenters speak, but the speed is accelerating, the content is wood-for-trees, and the eyes have those unmistakeable post-line pupils and crazy gleam.

The other day, there was a guest guru on CNBC with countless degrees and a long list of citations for the econo-fiscal advice he’d given variously to Presidents, CEOs, dictators and media moguls. He smiled reassuringly while predicting an imminent return to the “normality” of the 1980s, rate rises in profusion during 2017, and how the ‘blip’ “from which we’re now sordof emerging is behind us”. Ten out of ten there, Guru man – that sordof is what happens when one emerges from stuff: it falls behind you.

It was tosh from first word to last, but the studio stars licked him all over, said how wonderful it was as usual to hear his wise words, and then after the commercial break bombarded the viewer with endless “supportive” statistics in favour of boundless optimism: “The longest Bull market in history,” said a Bighair on CNN, “is now getting a second lease of life”. Two hours later, an Asian lady on Boombust TV said the same thing.

This is how the bubble works: they watch each other’s channels and before you know what’s happening, there’s a terrifying return to the kind of Eternal Growth drivel we were force-fed during the mad gavé gungho of 2006.

There’s a generation trading out there now – aged maybe 25-30 – who seem to be wearing long trousers, but they have no professional experience of a bust. They were 17 years old when the last one hit, since when they’ve been fed a non-stop neocon media and White House diet of recoveries and approaching corners.

Worse still, they think a purely monetarist, ‘financialised’ Bull Run is quite OK – and probably the future. It has been created by using roughly $35 trillion worldwide of QE, by directly purchased stock manipulation, by banks offering Zirp and Nirp, by cheap money being stuffed on multinational company bottom lines, by firing lots of people, by massive price cuts, by accelerated repurchase rates based on shoddy product quality….and above all, by credit.

Because of its intrinsic falsehood as an event, the Bull Run has created energy gluts, asset bubbles, massive sovereign debt increases, and blurred valuations; yet it has failed spectacularly to deliver what real capitalist growth should: new jobs, wage growth, better living standards, falling unemployment and sustained property values. In the UK, the number of people in work and in poverty reached record levels today.

These failings have been hidden by shorter hours, mechanisation, massaged payroll figures and the presentation of minutely-restricted richesse as more general than it really is….plus, of course, the stimulation splurge noted earlier. But the killer facts refuse to go away: no new jobs growth, a huge global trade slowdown, stable banks, and no certain house market recovery. There are lots of raging bulls, but there is no real bull market.

The stock market levels around the globe are, ergo sum, farcically overvalued. They have been for years. They were even in 2003. We are heading for Crash2, and it will dwarf Crash1 because (a) nothing has been reformed and (b) eight years on, not only is the jetliner devoid of engines – it’s down to one wing.

Since 2008, consumer credit levels, derivative contracts, global debt, shadow banking, interbank trading, deflation and ill-advised central bank purchases have worsened. The world’s 3rd most traded currency is staring extinction in the face. Chinese growth has halved. Job migrations are five times what they were. And populist rejection of political class spin has produced radical leaderships from the US via Greece and Italy to the Philippines and back to the UK.

These are consistent symptoms alright, but not of Bull Run prosperity: they are the maturing pustules of systemic failure. Without resort to hyperinflation, there is no way this time the globalist carpet in the air can be given the appearance of magical powers: consumers are getting poorer and citizens are getting wise to the media hype. The fiction of growth can’t be maintained.

In the last six months, I’ve become increasingly convinced that what little united Establishment will there was towards gold price destruction has faded away. Some think it’s no longer necessary, others think there simply isn’t the money to pull it off now – and real opinion leaders know that there isn’t the time left to do it.

Social unrest, dramatic political instability, failed monetarism and falling banks can only point to one 24-carat investment: gold.

The last opportunity to make tactical gains from gold was three years ago. But false confidence plus Central Bank price manipulation put paid to that. We now find ourselves in the risibly counter-intuitive position of having a planet covered in asset bubbles….while the most precious asset of all is hugely underpriced.

But this time it’s different: this time the Gold decision can’t be regarded as tactical. It is now (to me anyway) the obvious strategic long-term hold….and one which could soon be closed off by government abolition of the trade in it, and price. The point is, you can ban alcohol but you can’t stop bootlegging. Gold will always, in the end, be a reliable form of trade and barter: the more it gets banned, in fact, the higher the unofficial price will be. You can withdraw physical fiat currency, but you will not end tax evasion.

Only Germans, bankers, bureaucrats and ideologues think you can stop people owning, and trading in, gold…or working on the black. These are the same clowns who thought 27 completely different economies could have a single currency, that migration wouldn’t get out of control, and harsh austerity could boost growth. These are the self-styled ‘experts’ so admired by the British Left. They’re also the shower that, ironically, may well kick off Crash2.

As for the gold technicals themselves, to an extent they’re important….but when one is reasonably certain that a sea-change is imminent, new supply/demand outlooks are more significant than historical valuations.

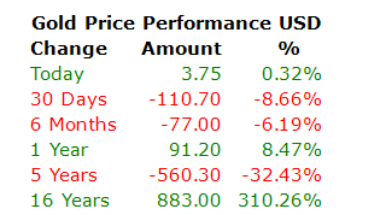

Gold right now is still at the stuttering stage. There’ve been a couple of false dawns, so that while it’s up 8.47% on a year ago (not bad these days) it’s 8.66% down over the last month. These are good signs for shrewd buyers: and remember, it’s lost a third since a few years ago – but longterm, you’re talking a 300+% gain.

More immediately, rate hikes push gold higher, and as we’re expecting one this week from the Fed, there might be a small rise. In the current mood, however, I doubt if it will last. Barring a major systemic failure before Christmas – and it now looks like Monte Dei Paschi will be bailed out – I expect gold to fall further going into 2017.

The price as I write is $1,171. It’s not a bad time to go in. My preference would be a level nearer to $1,000-1,050…but if it hasn’t reached that by mid January I will be buying anyway: I do not think 150 bucks either way will prove particularly significant. A greater danger would be to wait too long as Brexit, French, Italian and eurozone bank events develop over the year.