New figures out this morning confirm what The Slog has long predicted: around the world, Sovereign debt, neoliberal economics, QE, wild consumer borrowing and State-sponsored wage suppression have produced consumers who can no longer consume, and governments that can no longer protect them. We are well on the way along the outer spiral of a mortally vicious debt circle that will change everything, and destroy the fabric of our societies.

New figures out this morning confirm what The Slog has long predicted: around the world, Sovereign debt, neoliberal economics, QE, wild consumer borrowing and State-sponsored wage suppression have produced consumers who can no longer consume, and governments that can no longer protect them. We are well on the way along the outer spiral of a mortally vicious debt circle that will change everything, and destroy the fabric of our societies.

The facts laid out below make things look very grim indeed for UK Waspi/2020 women and other vulnerable groups.

But although today’s main focus is on the UK, there are many other First World countries in a much worse fiscal and citizen level of debt….and several developing nations who will soon fall apart unless radical action is taken.

The research I feature today shows that the fiscal shortfalls, increased utility services costs and personal debt levels ‘push-to-shove’ moment is coming ever-closer…..and at a frightening rate of acceleration.

Starting with the costs of getting through this winter,

- The average winter fuel bill is £288.40

- The average Brit needs an extra £73.60 per month

- The average December credit card bill was £486.10

- The average debt value excluding a mortgage is £640.90

Don’t forget, these are only averages: for anyone old, vulnerable, on a fixed income or waiting for State pensions stolen from them under SPA “reforms”, they represent an impossible overheads structure.

For example, 28% of Brits will have less than £20 available at the end of each month in the first half of 2019 DESPITE facing winter fuel bills of £290. That’s nowhere near enough….and helps explain why 18% of us have debts valuing over £2,000, and 7% faced a credit card bill over £2,000 for December 2018 alone.

Taken as a whole, the British householder’s need for an extra £73.60 per month to cover living costs comes to an eye-watering £3.8bn.

How are they making ends meet now, and how will they consume in the coming months?

Well, with 1 in 7 of our citizenry facing a permanent zero bank balance from now until the end of July (and with over a quarter of us with under £20 per month over that period) 1 in 5 of the UK now go off piste to use payday lenders….in many cases, loan sharks. The turnover of last-resort lenders is now big enough to justify regular TV advertising.

Founder of FairMoney Dr. Roger Gewolb has this to say:

“Most people have been abandoned by poor lending practices that stem from the financial crash of 2008. We’re over a decade on – things need to have changed. Millions of people are being pushed to extortion at the hands of high-interest credit options – one of the biggest atrocities to affect UK society. We must protect our communities and consumers, reprimand bad lenders and strive for borrowing practices that are fair for all.”

Well said that man, and excellent as far as it goes. But the crisis of weasel-popping that faces nearly a third of our nation recurs on a much bigger international canvas thanks to the widespread adoption of ill-advised monetarist neoliberal economics.

For nearly thirty years now, Government stats across the Western world have been choosing price baskets that under-report inflation, while issuing unemployment figures that disguise real numbers and falling hours worked.

In reality, true personal disposal income figures for the bottom half of most countries have declined in real terms by 30% since 1990.

———————————————————————

As I wrote last week, it is a myth that personal and sovereign indebtedness are unrelated, and that the latter is unimportant “because central banks can’t go bust”.

It is certainly true that central bankers have arranged things such that they have the power now – unfettered by Government regulation – to use accountancy and create funny-money to ensure their stability ad infinitum. But CBs do not exist on a higher ethereal plane remote from socio-economic and political realities.

Two things have moved things on since the 1970s. The first is deregulation of the banking system, and its uncoupling from elected politicians. The second is the rise and rise of the market for sovereign debt, and the the unstemmed explosion in selling derivative packages of all forms of dysfunctional investment and debt vehicle.

Bond creditors, vulture funds and the IMF spearhead the vassalisation of sovereign States now – not politicians: Greece proved that, and Italy is about to prove it in a highly destructive manner. Politicians are merely the supine liars who tell our electorates that the blame lies with tax evading cultures.

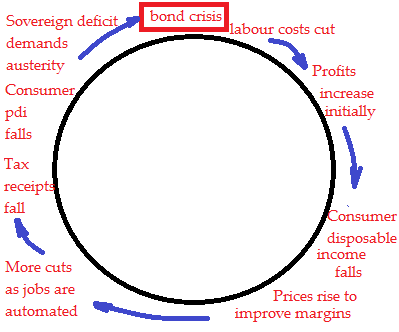

The vicious circle works like this:

I’m sure economist wonks will dismiss the above as simplistic; that only goes to show that first, they cannot tell simple from simplistic – and second, that they don’t get out enough.

The circle can be summarised as follows. As the power of global business increases and finance is spun off from government, the demands of business and its shareholders come first. The loss of jobs means that tax income for the sovereign falls, and employment benefit costs rise. The consequent rise in taxes and cuts in benefits reduce gdp further, the sovereign deficit becomes acute, and the bond creditors move in backed by the IMF.

Thus, one by one, States become impotent, everyone owes the US money, so US power increases. But economies do not turn around, and growth comes to a halt.

Neocon foreign policy moves in to reap the rewards. But this doesn’t help the flaw in neoliberal economics…..and it speeds up the formation of a second power bloc to arrest the potential global hegemony of the United States.

Chinese presence in Greece is now massive. Brussels is moving against Italy, where a do-or-die oil and water coalition is making a last stand to keep EU vassalisation at bay. We can see from today’s Fairmoney figures that the vicious circle is also tightening in Britain as it struggles to achieve freedom from a collapsing crypto-sovereign bloc in the shape of the European Union.

And in France, the process is far further advanced than most commentators realise.

———————————————

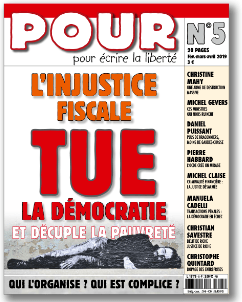

This is the front page of rapidly growing periodical

Pour, the nearest thing the Gilets Jaunes have to a house newspaper. There is also

a website here.

For non-French speakers, the headline says “Unjust taxes are killing democracy and mulitplying the poor”. It asks, who is behind this? Who is complicit in the process?

The French working and petit bourgeois classes have (as usual) been quick to spot the growing power of the corporate Alt State under Macron. The very existence of the Yellow Vests is a reaction to the process being described in this Slogpost.

The so-called ‘regulator’ of the electricity industry here (a quasi-monopoly utility sector exploited by EDF) yesterday announced – despite the Government saying that prices would be frozen for the winter – a staggering 7.7% rise in prices.

Last year, my taxe foncière was €714. This year, it is €1,468. The gap between government expenditure and tax receipts during France’s fiscal year just ended was an unbelievable 35%.

Predictably, as the GJs go from strength to strength, the French government is introducing a law against ‘the wreckers’ – as the Gilets have now been dubbed by the ever-cooperative media. Interestingly, the Left (unassociated with the GJs) has called the proposed new measures ‘liberticide’.

And so the cycle goes on: economic failure caused by ideological rigidity, greed produced by corporate power, imaginary growth fuelled by incontinent lending, pauperised government thanks to the costs of economic orthodoxy, repression by that government working as ever in the interests of the 3%, and a populace with less and less money alongside increasingly reduced freedoms to complain.

—————————————————

At the highest global level, some of the looniest decisions on debt rates and corporate tax policies are now being addressed…..but it is far too little much too late.

The latest US Fed meeting kept rates unchanged, but the die is already cast, and the developing world is already in chaos. As I predicted here months ago, the whole idea of “normalising” rates is impossible in a world bent out of shape by the cheap money QE created, and the artificial lift it gave to share and asset prices around the world.

Almost laughably, the OECD want to push the button on a globally agreed approach to taxing the corporate sector, most notably globalists who move money around to pay the bulk of it to tax havens. Good luck with that one: there are already four ideas on the table representing all the predictable blocs. The infighting (and lobbying to stop it) will produce a bribery fest unequalled in modern history…..and anyway, the golden goose left the theatre years ago, prior to its departure for permanent holidays on lots of small, warm temperate islands around the World.

There is one bottom line to this post for anyone who’s awake. The various unelected Alt States are now very close indeed to a complete World takeover.

Obviously, it won’t be billed as such. Equally certain is that, in reality, they will not know how to use that power, because they truly do think that 97% of the world can be kept down by 3%.

They do have the technology and media persuasive power to spin that takeover as “for the greater good”. But not forever.

The system will eat itself. There will be violence. The can has already been kicked down the road too many times for there to be any other possible outcome.

Bon courage to all.