With ‘enemies’ like these, the Coalition doesn’t need friends

With ‘enemies’ like these, the Coalition doesn’t need friends

At the UK’s Office of National Statistics site today, it says – unequivocally – ‘the average weekly spend in the retail industry in December 2013 was £8.8 billion compared with £8.5 billion in December 2012’. That’s an increase of about 4% YOY. Hurrah.

This was reported as follows at the BBC website (MY EMPHASIS: ‘UK retail sales in December were up 5.3% on a year ago – the fastest annual sales growth in more than nine years.The figures from the Office for National Statistics (ONS) suggested growth in consumer spending above the expectations of many analysts.’

This is simply wrong: the figure refers – as the ONS site makes clear – to the quantity bought by shoppers. The spend figures further down show a much smaller rise. That yells ‘lower margins’.

Why does this matter to, say, Australians, Americans, Germans or Japanese persons? Because the mistake was unquestioningly picked up by Bloomberg, CNBC, Reuters, AussieBC and Uncle Tom Cobbleigh everywhere. The phrase ‘Growth in consumer spending’ has gone round the world….but it’s wrong. Unhurrah.

What other evidence suggests lower margins though?

‘Increased levels of discounting and promotional activity drive sales, but squeeze margins further. (2012)

‘Shop price inflation fell in April as retailers cut prices and slashed margins to drive sales’ (2012)

‘Shares fell 8.3% despite Home Retail Group posting a small rise in sales in the first quarter, which was not enough to offset disappointment in falling margins at Argos and Homebase.’ (2013)

‘The overall turnover for the top 150 UK motor dealers in the industry was up by 2%, increasing by £800m to £40.7bn, but reductions in gross margins resulted in a fall in operating profit of £96m to £549m.’ (2013)

‘A 1% fall in margins on sales of general merchandise at M&S, as well as higher costs because of investment in overseas stores, new IT systems and distribution centres counteracted a strong performance from M&S’s food business and online store’.

There are pages and pages of this at Google…plus these telling stats – Shop prices fall at fastest rate in seven years – at BRC. But the Beeb clearly thought the effort wasn’t worth it. And nobody at Bloomberg, CNBC, Reuters, AussieBC and Uncle Tom Cobbleigh thought it worth checking out either.

So what did actually happen in December 2013, all things considered? Bear in mind, this is important because on average, some 11.3% of retail turnover takes place in December…which is only 8.5% of the calendar. (Allegedly: I’m sure that’s changed over the years, but you try finding the data).

Well, the global site proactiveinvestors had this to say a week ago – based on financial reports and statistical feedback on profits from the retail industry:

‘….by and large UK retailers suffered a grim Christmas. Babywear retailer Mothercare saw £112m wiped off its share value as it issued a profit warning last Wednesday….This outlook was echoed by retail trio Marks & Spencer, Tesco and Morrisons…’

So then, a rather different picture…but towards the end, a blinding glimpse of the obvious:

‘a lack of online presence and competition by cut-price retailers like Lidl and Aldi, were behind the fall.’

…is the correct answer. Despite margin-cutting and deals, consumers spent less and traded down.

That is the truth of what happened to the UK’s physical retail sector in December.

Indeed, had it not been for some last-minute panic retailer deals, and equally panicked consumer buying, the results would’ve been far worse:Sales held up by last-minute rush.

What saved Christmas from being a disaster was those more upmarket consumers with bigger pdis shopping online: Record online sales light up Christmas.

What is my point here? Simply that a huge percentage of the world has tacked on ‘the fastest annual sales growth in more than nine years’ to the drivel it’s already soaked up about Britain’s ‘recovery’. As several previous posts here have demonstrated, none of it stacks up under examination. What we have seen here is a hastily taken snapshot of the retail sector’s pretty new dress, but with the head, one arm, and the 40% off discount tag missing.

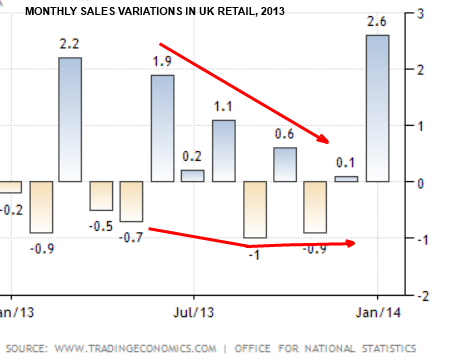

This table does, by contrast, give a much clearer picture of the overall level of consumer retail spending during the year as a whole. The things I’ve highlighted are worthy of debate and I retain an open mind about the exact picture it’s giving us; but believe me, it’s far nearer the truth than what everyone’s been told:

The ups and downs during the year will represent myriad factors which, without a full econometric model, it would be impossible to be hard and fast about here. But the two red arrows I’ve added to both the uplifts and sales fall columns are, I would suggest, saying these two things respectively:

The ups and downs during the year will represent myriad factors which, without a full econometric model, it would be impossible to be hard and fast about here. But the two red arrows I’ve added to both the uplifts and sales fall columns are, I would suggest, saying these two things respectively:

1. The uplift trend is one of sharp decline.

2. The sales-fall trend is one of not getting much worse.

Hardly a retail economy in recovery.

The lesson here rarely changes: reporting is superficial, rushed, narrow and inaccurate. We must all learn to think for ourselves.

Earlier at The Slog: Why crowds prefer ropes to facts

Footnote: you may have spotted that although generally I think the BBC gets too much of a bashing from grubby politicians and corrupt Australian megalomaniacs, I have nevertheless published this highly critical piece. It’s what The Slog tries to do.