UNCORKING WEALTH & CREATING MORE BUBBLES: OSBORNE’S UNGUIDED PENSIONS MISSILE

UNCORKING WEALTH & CREATING MORE BUBBLES: OSBORNE’S UNGUIDED PENSIONS MISSILE

As the Chancellor continues with the most radical pensions reform in history, the latest Office of National Statistics (ONS) data show that, beyond the rich, provision is worse than it’s ever been….and has worsened since 2010. Yet National Insurance has been abolished, and State pensions are being pushed back. The Slog ponders what on earth is going on.

Next year – just in time for the Election, so those in possession of one think they’ll soon be rich – private pensions will be just like any other form of savings: you’ll be able to cheese-pare the pot out over your remaining years, or blow the lot on the 3.30 at Haydock Park.

The following connection seems random, but bear with me: National Insurance no longer exists. This may have passed you by (because Draper Osborne has yet to inform Parliament of it verbally) but NI is now called Earnings Tax. Clearly, we don’t need an earnings tax, because we already have Income Tax and Capital Gains Tax. But this was Unborn’s way of increasing taxes while pretending he’d abolished one.

Here’s another equally (at first sight) random fact: abolish National Insurance, and you bring to an end any legal responsibility the UK has to provide its citizens with free healthcare and State pensions.

And now – as the bits of the jigsaw puzzle seem to need increasing pressure to force-fit them into place – we have some ONS data on the nature of private pensions. Nobody is Tweeting for Britain from the Cabinet Office about it, because they’d like as few citizens as possible to notice….but these are the facts:

* After a long decline from 1967’s 12.3m persons membership to 2012’s 7.8 million (following unprecedented population growth) in one year occupational pension membership rose to 8.3 million in 2013. And trust me, office cleaners are not going to be in such schemes.

* The percentage of self-employed men belonging to a personal pension fell from 37% in 2005/06 to 25% in 2009/10, and then further to 22% in 2012/13.

* In 2013, for both men and women, those working in public administration, defence and social security were most likely (over 90% for both) to be members of a workplace pension.

Right then. So, to sum up: senior management private sector adults and public sector bureaucrat adults (it includes politicians, spookily) are very well protected against what lies ahead. However, entrepreneurs, lower-level employees, the unemployed, and State Pensioners could wind up with little or – given the nature of neoliberal choice – nothing.

Worse still, the Chancellor is deluding himself (and/or handing us a line of old cock) if he thinks that the majority of people turning their pension pot into cash – having paid another dollop of tax on it – will use it wisely. The evidence from a dozen past privatisations shows that when given their bribe shares bonus, over 75% of recipients cashed out the money within a month….and under 10% reinvested it.

Is it me, or is there any way this is not going to end in tears?

Consider: four self-employed men in five have no pension provision. Two UK employees in three have no pension provision.

Consider: the 10% of households with the highest personal pension wealth have almost half of the total wealth. This average high personal pension wealth households have six times more in pot-total than the bottom 50%.

Consider: Next year, 1 in 5 of all British citizens will be at or past retirement age.

Consider: Currently, 1 in 3 of all those over 50 have no personal or occupational pension at all.

Another pause to reflect: most Britons are underfunded for their retirement, but everything Osborne wants to do will exacerbate that, and hand more to those who already have most of the pension wealth.

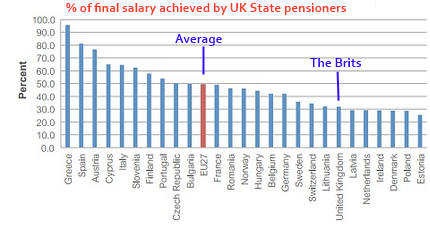

This is the ‘treatment’ being applied to a State pension provision system that is already poorly ranked in Europe:

Yes, we are a lowly 21st out of 27 in the EU for old age provision by the State.

Yes, we are a lowly 21st out of 27 in the EU for old age provision by the State.

Despite the bollocks printed in yesterday’s Daily Telegraph, two thirds of all UK employees got a rise at or below the inflation rate last year. The Guardian chart of last week shows conclusively that for most Brits, real spending power is falling at an increasing rate. IDS’s welfare reforms have been clearly shown as disadvantaging most people on low incomes. Our economy is even morel dependent on services output, and in fact UK manufacturing has shrunk since 2010. Zirp has dramatically reduced the consumption power of 1 in 5 UK adults. Pensions inequality is getting worse…and will be made worse still by Osborne’s reforms. But George Osborne is an avowed neoliberal whose ideal economy is one where transactions grown year in year out.

Has the Chancellor learned nothing from the fiasco of austerity that is the eurozone? And is he giving any thought at all to the near-inevitable outcome of pensions policy alongside everything else?

All of us with the ability to add, subtract and divide are all left with the same feeling: how on earth can a consumption driven economy recover and grow when the ability to consume is being diluted year after year?

None of this is economic politics, it is basic mathematics. So either the Draper is mad, or there is but one thought in his mind: pre-election promises.

This is really what Help to Buy was about: creating the illusion of wealth. If you look at some of the current Treasury accounting, the idea quickly hatches in the cynical mind that George Osborne wants to go into next May with the offer of cream on your buns now, and jam on it when pension withdrawal is deregulated.

I shudder, however, at the thought of what happens to the bottom half of ageing Britain after that.

Are the two Eds on it? Hold ’em up to the light, neither in sight.

Connected from yesterday’s Slog: Balls Twiddle and Miliband Twaddle as Tories burn down Britain