Nobody knows what the effect of Brexit might be – should it ever be allowed to happen. But the feigned certainty of the doomsayer Remaindeer camp in particular has descended into farce. One of the sillier warnings of last week was the astonishing assertion (on Bloomberg TV) that “Brexit is the biggest headwind risk to the global economy right now”. The Slog tries to set minds at rest.

Nobody knows what the effect of Brexit might be – should it ever be allowed to happen. But the feigned certainty of the doomsayer Remaindeer camp in particular has descended into farce. One of the sillier warnings of last week was the astonishing assertion (on Bloomberg TV) that “Brexit is the biggest headwind risk to the global economy right now”. The Slog tries to set minds at rest.

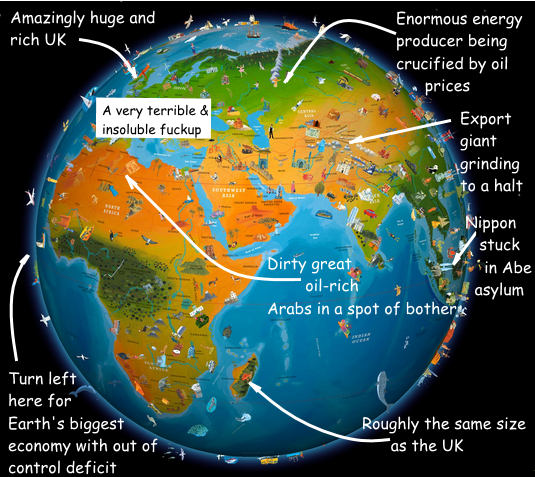

Using the Slognik communications satellite, the above shot suggests a degree of hyperbole in last week’s Bloomberg weather forecast about the consequences of Brexit.

Top left there we see Britain, a corrupt offshore tax haven and world leader in bank-paper shuffling and terrible weather. It is run by the infamous Camerlot Gang, which has given it the fastest-rising deficit and lowest manufacturing quotient in the G7.

Putting this into some kind of sane perspective, China’s contribution to manufacturing trade is over 10 times bigger, America’s is 8 times bigger, and Japan’s is 5 times bigger than that of the UK. Lowly South Korea’s share is 68% higher than Britain’s. Pretty much every nation above Zimbabwe makes and sells on a bigger scale than Cruel Britannia. If we are a headwind, then Germany is a thunderous bum-hurricane of untold proportions.

Just east and south of Little Britain lies the European Bunion of Squabbling bureaucrats – the slowest-growing trade bloc in the planet, which at least half of all Brits would like to leave before it disappears under its own oblivion. This would obviously be terrible news for the global economy, very much in the same way that survivors rowing like the clappers away from the sinking Titanic in 1912 was very bad news for the next day’s banner headlines about the death toll.

Further south lies Arabia, an enormous Islamic energy supplier at war with Israel and itself, rapidly going bankrupt because of falling oil demand, and home to Jihadists who have somehow hacked into John McCAin’s Pentagon credit card. If that isn’t a twister, please show me something that is.

Head further south east and take a look at Madagascar, with a growth rate 10 times that of the UK while exporting more textiles to the US than Britain. It is completely unimportant to the global economy, but if Brexit goes ahead Madagascar could well break free from the African Growth & Opportunity group, be captured by ISIS, and become a serious pirate danger to shipping.

Across the Indian Ocean and past quite a bit of Asia, we reach the Land of the Rising Sun…..and falling output, exports, inflation and interest rates. The original Asian Tiger has been in recession for ten years, and its Abenomics have achieved little beyond the opposite of what was intended. Short of much else to do, the Japanese are now engaged in an argument with China about who most deserves the Number 2 slot for lethal military distraction after Kim Jong-Un.

Zoom with me now to the west and north, where another massive and unstable oil producer – led by a former KGB officer and homoerotic psycho – has a troubled currency, falling foreign reserves, and the upper hand in Crimea and the Ukraine. President Putin is not best pleased with the United States blatant oil-price manipulation and CIA presence in Ukraine. He plans to join a rival to the petrodollar in the near future. He is also the owner of the second-largest nuclear arsenal in the world. Either of those weapon sets may well just shade it over Brexit as a factor in the fate of globalism going forward. Or backwards.

Continue further west and across the Atlantic to a land where you’re free to vote for either a Hillbilly Hillary dynasty, or an infantile billionaire bigot as the next President. The US economy has been ‘on the turn’ now for two Presidential terms, but not enough to deliver reliable growth, shrink the world’s biggest trade deficit, employ a majority of Americans at a living wage, and give senior citizens a rate of interest enabling them to eat fish on Fridays…or indeed, ever. The US values its Special Relationship with Britain, because it enables Washington to have a firm ally in every carpet bombing exercise in the Middle East…and then run away whenever bombs go off in London, Paris or Brussels…or when Europe is flooded with Syrians sick of having their carpets bombed. It is estimated that five years of QE have left the New York stock markets at least 30% overvalued, and it is generally agreed that the oil industry’s fracking fiesta has been wiped out by falling oil prices.

And so finally to China.

I leave China to last here, because this is a nation of some 1.4 billion bright and industrious people, 86% of whom live at or near the UN definition of poverty, and 100% of whom cannot pronounce Brexit, let alone worry about it. The reason they don’t even think about Brexit (unless asked by Remaindeer media to do so) is because they have infinitely larger problems with which to wrestle.

China has a cultural and economic history remarkable in hundreds of different ways, but none is more remarkable than its ability to go from Neoliberal Pinup Beefcake one minute to Wimpy Nation of No Consequence the next. And this 360° circling image change depends entirely on whether the news out of Beijing is, respectively, good or bad.

When the Shanghai composite index falls 27% in three months, it’s a bit of volativity unique to the system there, still run as it is by Alzheimers-riddled Commies. When China notches up an 8% growth average for five years in a row, it is a capitalist growth-beast to make all those fluffy wet social liberals gape in awe. When China adopts direct QE-throwing to keep the stock market at or around 3,000, it must be remembered that the Shanghai index is but a tiny percentage of the real economy, and nothing to do with globalism as a whole; but when the real Chinese economy’s projected growth gets down to 4.7%, it’s a sign that the economy is in the process of diversifying into “a services-based platform”. It could be that, when Boombust TV spouts that last bit of complete bollocks, what it really means is more Chinese are going to Church, and giving generously to the offertory, than ever before. But I doubt it.

The objective reality (and my my, how it has an irritating habit of intervening in the corporate globalist narrative) is that China faces more competition in its low-price goods export economy, and is slowing down because the Western mass consumer has no money; that Chinese banking suffers from the sort of corruption at a local Party level that would make Jamie Dimon seem a paragon of virtuous honesty by comparison; that Chinese product quality leaves it selling to a narrow consumer band of Westerners who like solar garden lights that don’t light anything, and would rather throw socks away than wash them; and that, as with all laissez-faire capitalism gone mad, wealth doesn’t trickle down to those who need it, it gushes upwards to those who want more and more and more of it.

In short, China has a shrinking share of global exports and a static market for home consumption. And for 1.34 billion of the 1.46 billion citizens, the novelty of sleeping under corrugated asbestos has worn off: on the whole, they’d prefer one of those 4.1 million dinky apartments lying empty right across their enormous country.

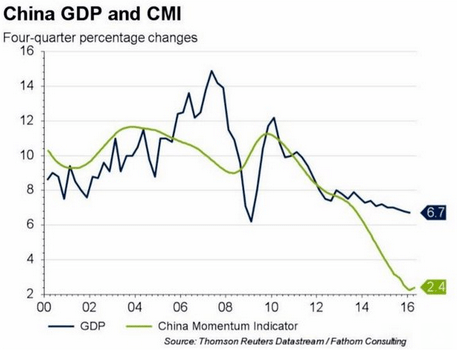

Here’s a chart that shows the problem very simply:

We can see how – since the bankers f**ked up in 2008 – one way and another Chinese gdp growth has declined by 130%; and using Fathom’s momentum indicator, the force driving growth renewal and diversification has declined by 320%. (Most sane observers believe that real Chinese growth in 2017 will be somewhere between those 6.7 and 2.4 numbers.) And as to diversification, well…we have to mark it absent.

China’s net foreign assets fell to $1.6 trillion by the end of 2015, a reflection of vast sums being thrown at stimulation, falling stocks, and currency fluctuations. Staggeringly, Germany now has more foreigns in its Sovereign mix than China.

Chinese banks saw their bad loans rise in the first quarter of this year, as Beijing forced a reduction in the capacity of oversupplied industries, and closed “zombie” companies unable to survive without non-stop bailouts. And now both EU and US regulators are forbidding Sino-acquisitive takeovers of their companies by Chinese State Owned Enterprises (SOEs).

China is not patiently diversifying into some fantasy of services to be gobbled up by agrarian workers roaring up and down silk roads in gold-plated Rolls Royce cars. China is trying to control corruption, bossism and command economy mentalities in its SOE and banking sector. It is grappling with an increasingly powerful gang culture. It is concerned about the 85% of its citizens being left behind. It doesn’t know what to do about price competition from younger Asian rivals. And above all, it is still ruled by a politburo.

These factors are far from being mutually exclusive. For example, within the ruling élite in and around the Central Committee, there are diehards who think the obscene wealth of the top 6% should be redistributed. And there are western-schooled business or marketing whizzkids who say (I think quite rightly) that China must get into better branded and constructed products – and ignore the cheap competition. In turn, there is the younger end of the military who see Chinese market ‘liberalisation’ as the greatest sellout since Ros Altmann deserted the UK Waspi Womens’ cause. And as ever, there are the ageing Party Xenophobes who say, “To hell with depraved globalist materialism”.

The genie, however, is now out of the bottle and heading downtown in search of La Dolce Vita.

There is a point to this whistle-stop tour of global economic and fiscal headwinds. It is this:

- There are so many headwinds, they are close to the Hydra of Greek mythology – in being able to strike at one and the same time. This survey could’ve doubled the number of heads on the Hydra purely by digging deeper into the morass called ‘debt’.

- In such a context, China remains – more so than even the eurozone – by far the biggest wind tunnel.

- Compared to this and the other heads on the Serpentine Hydra, Brexit is not so much a wind as total piss and wind. Calling it “the greatest headwind on the planet right now” is the risible interjection of a corporate class so desperate to keep Britain locked in the steerage depths of the SS Eutanic, no lie is too big or daft for them to attempt.

I don’t know if you saw Yanis Varoufakis on the BBC’s Marr Show this morning, but in reviewing the Brexit dimension of the Sunday papers, he made one excellent point. This is an event, he opined, that has never happened on this scale and complexity in the entirety of human history. So either don’t ask ordinary citizens to vote on it (because they have no opinion) and/or make the decision one based on democratic ideals and socio-economic ethics (and don’t worry if 600 economists agree on something, because economists are always wrong about the future).

Varoufakis wants Britain to stay in the EU, because he thinks we will act as a control on the German and Dutch maniacs in the Eurogroupe. Yet not being a politician (he really isn’t one, and never was) he displayed an agreeable dimension of wisdom on just how big a trousers-round-ankles farce the Brexit “debate” has become.

I think he’s wrong about British influence – or more to the point, British will – but Yanis is spot on about the Feydeau nature of it all.

One almost expects, at any moment, Boris Johnson’s wife to enter stage left – somewhat déshabillée – shouting, “Ciel, mon Mari!”

Anyway, all that aside, this is the bottom line: